- Independents and small public E&Ps active in US shale cut $17 billion with each company cutting 35% on average while the major E&Ps capex revisions average 20%

- Budget cuts announced to date are expected to result in about half the number of new wells drilled and about 40% reduction in completions activity in 2020 compared to 2019, assuming no additional capital revisions

- With little visibility of oilfield service revenue beyond May onwards in 2020, the supply chain has to prepare for the worst as E&P budget cuts may continue

US Onshore E&Ps Cut 35%, $17 Billion, of Capex from 2020 Plans

In March, 34 out of the 51 (67%) public E&Ps active in the US announced capital expenditure (capex) cuts totaling $33 billion.by . These revisions will have a dramatic impact on the drilling and hydraulic fracturing supply chain – causing rapid readjustments across the industry.

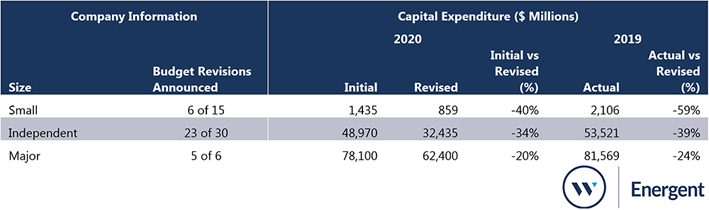

Table 1: Summary of capex revisions by E&P size

Source: Westwood D&C Outlook

The percentage cuts announced to-date are largest for the smaller E&Ps which have averaged 40% so far whilst larger Independents have cut 34% and the Majors 20%. Together small E&Ps and Independents account for $17 billion of capex reductions compared to the majors $16 billion. The cuts by the Majors cover their global operations but a significant proportion of the $16 billion cut will be in the US. Several Independents including Centennial Resources, Continental Resources, and Murphy Oil all cut their initial capex by at least 50%. The major’s capex revisions range from 11% reduction by ConocoPhillips to 25% decrease by BP. ExxonMobil is the only Major yet to announce a revised budget.

2020 capex was already planned to be lower than 2019 before the crash happened and so the revised 2020 capex plans are down 59% for small E&Ps and 39% for independents compared to 2019.

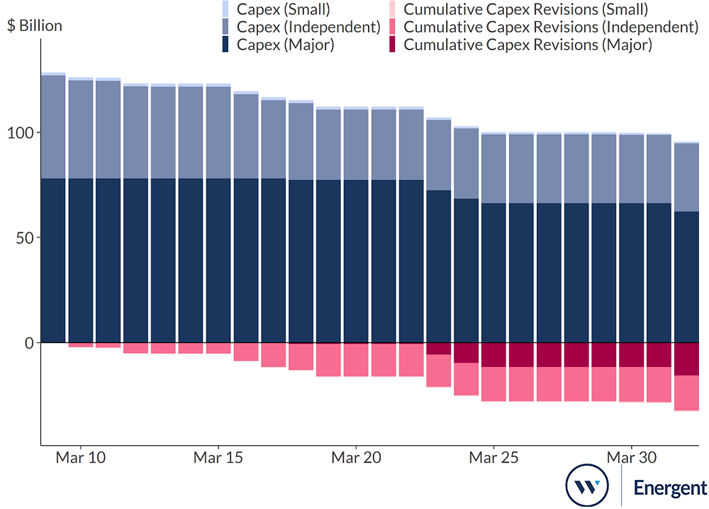

Capex Revisions (2020) US-Active Onshore Public E&P's

Figure 1: Change in capex level and revisions amongst companies who have revised their 2020 capex

Source: Westwood D&C Outlook

Of the 17 public E&Ps yet to revise their 2020 capex, 8 were majority natural gas producers in 2019 with approximately $4.5 billion of unrevised 2020 capex. Some gas producers have cut but by lower percentage amounts. Both EQT and Range Resources cut their initial 2020 capex guidance, with EQT, whose 2019 total production was 98% gas, cutting by only 6% compared to Range Resources’ 17%, whose 2019 total production was 69% gas and 28% NGL.

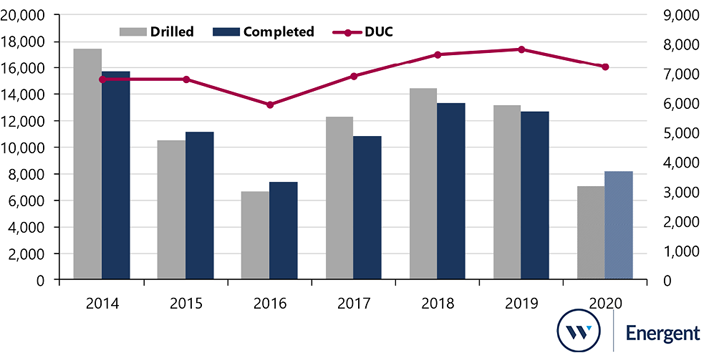

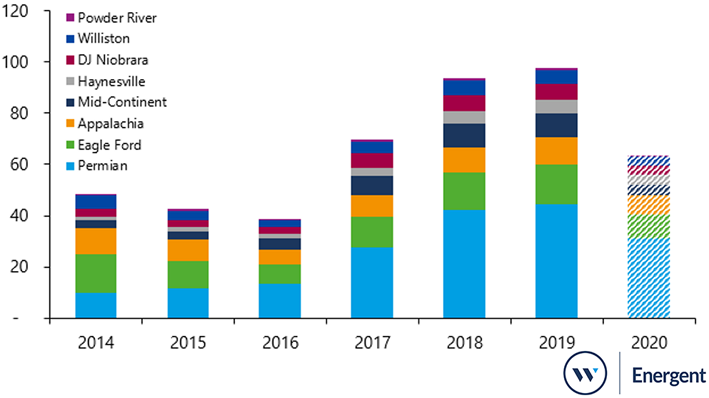

US Horizontal Drilling to Decrease by Half and Completions by about 40% In 2020

Westwood anticipates further spend reduction from public independents, small E&Ps, and private equity-backed operators. The independent E&Ps are aggressively reducing planned rigs for 2020. Continental Resources reduced rigs by 64%, Ovintiv cut rigs by 70%, and Pioneer lowered by 50%. The median rig decrease is 58% for 2020 across the E&Ps that provided rig guidance.

Overall Westwood expects drilling to be reduced by half and completions by nearly 40% in 2020. The number of wells drilled and wells completed are immediately impacted by the capex cuts as E&Ps stop work to reduce spend.

The most severe rig count changes will take place in the Permian basin as it makes up nearly 60% of the total land rig demand. Rigs not under long term contracts are expected to be the first to be stacked along with rigs working for primarily independents, small, or private E&Ps.

Figure 2: Horizontal drilling and completions revised outlook

Source: Westwood D&C Outlook

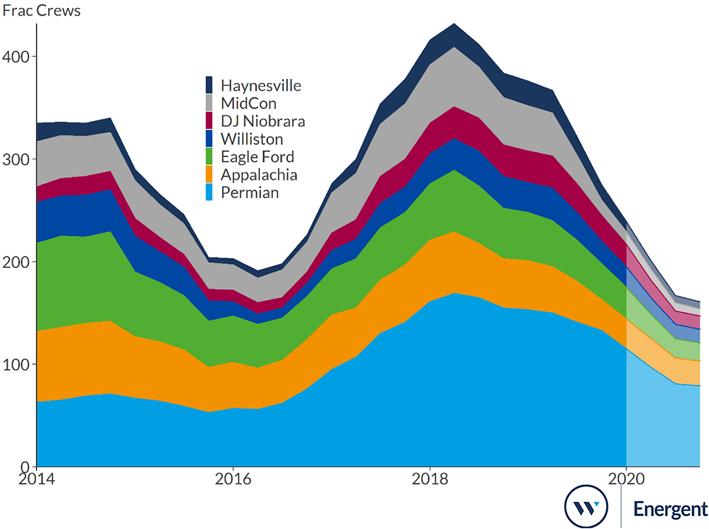

Frac Crews Drop by about 40% by the end of 2020

New E&P capex guidance presents an immense challenge to pressure pumping companies -a sector already hard-hit by E&P capital discipline and divestiture.

Hydraulic horsepower (HHP) demand for horizontal wells in the Permian fell from 6.1 to 5.4 million HHP from Q1’19 to Q4’19. By the end of 2020, Westwood forecasts HHP demand in the Permian to fall by another 2.5 million HHP, reaching 2.9 million HHP. Total Permian frac crews by then would hover around 70 to 80 – having previously been near 133 in Q4’19.

So far, two large pressure pumpers have revised their 2020 capex. Schlumberger reduced $510 million (30%) from its initial 2020 capex guidance of $1.7 billion, and NexTier reduced $100 million (48%) from its initial 2020 capex guidance of $210 million.

Other companies, such as Halliburton, have signaled their intention to significantly cut their initial 2020 capex guidance and laid off 3,500 employees. ProPetro, who had 22 active frac fleets all in the Permian at the end of 2019, notified state authorities of 388 layoffs at its Midland facilities in March. Also, in March FTS International laid off nearly 200 employees as the company reconfigured to meet lower HHP demand.

Pressure pumpers will continue adapting to this new reality. Westwood anticipates the total frac crews across all major US onshore basins could drop from 275 to approximately 160 crews from end of 2019 to the end of 2020 – a fall of 41%.

Figure 4: Frac crews revised outlook

Source: Westwood Horsepower Outlook

Frac Sand Suppliers Curtail Production

For 2020, Westwood forecasts frac sand demand to decline about 40% from 2019 totaling approximately 60 million tons. On a quarterly level, second quarter of 2020 proppant demand is forecast to decrease dramatically to approximately 16 million tons. This is about a 20% decline, the largest dip the industry has seen quarter over quarter. By the end of the year, frac sand demand should begin to plateau around 13 million tons per quarter. This new frac sand demand profile will bring more changes to the sand supplier landscape.

Figure 5: Lower 48 proppant demand (million tons)

Source: Westwood Frac Sand Outlook

Many frac sand suppliers will begin to curtail operations to protect balance sheets. Already, Covia Corporation announced idling of 15 million tons of frac sand supply and exited rail car lease agreements to reposition the company’s energy segment. Other frac sand suppliers will be vulnerable, especially those with operations in the Mid-West or multiple in-basin mines in the Permian or Eagle Ford.

Using Mine Safety and Health Administration data, the Mid-West mine utilizations declined by 19% from Q3’19 to Q4’19, the largest decline in utilization on a region level as they continue to battle for market share with lower cost in-basin sand mines.

Key suppliers, such as Black Mountain Sand and U.S. Silica Holdings were two of the first to publicly announce operational updates after the oil price crash. Black Mountain Sand devised a continuity plan which includes the company to “manage discretionary costs to run as lean as possible.” U.S. Silica, on the other hand, is idling a 1.5 million ton per year plant in Sparta, Wisconsin. Westwood expects mine productivity to decline by 30% or more for companies to scale back operations.

Limited Visibility in an Uncertain Market

Across the supply chain, companies will have to adapt and reconfigure to be able to survive the current low-price environment with falling order books and pressure on pricing. Oilfield service companies most at risk will be those who lack the ability to cutback services while maintaining enough cash flow from operations to continue.

The E&P companies’ capex is the supply chain’s revenue and the ramifications of 35% capex cuts are immense for the oil field services companies. Survival will be the key theme for the supply chain in 2020.

Todd Bush, Head of Onshore

tbush@westwoodenergy.com

KeyFacts Energy Industry Directory: Westwood Global Energy

If you have news or commentary you would like to share, please contact us and we will be in touch.