Tower Resources has received an updated independent Reserves Report from Oilfield International Limited ("OIL") on behalf of the Company's wholly owned subsidiary, Tower Resources Cameroon S.A, covering its Thali production sharing contract, offshore Cameroon (the "PSC"). The 2020 Reserves Report, which conforms to SPE_PRMS guidelines, does not contain new technical information compared with the previous report prepared by OIL and announced by the Company on 1st November 2018, but the 2020 Reserves Report reflects updated prices and costs reflecting the changes in the market over the intervening 16 months or so.

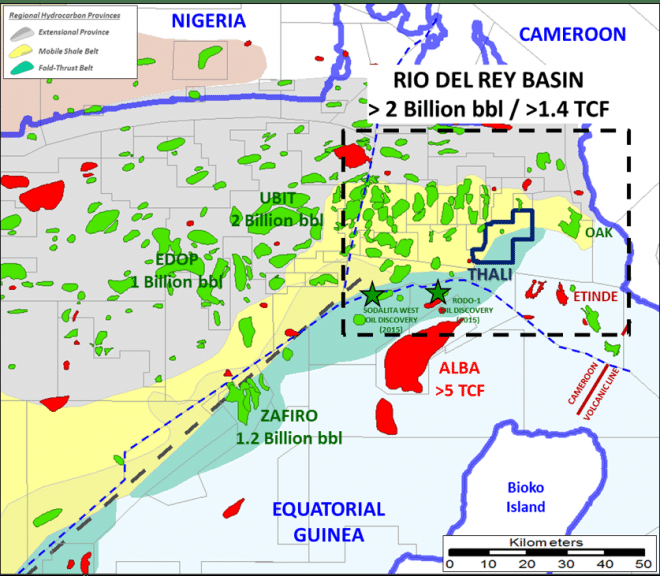

Map source: Tower Resources

The 2020 Reserves Report, like the 2018 Reserves Report, has quantified contingent and prospective resources across multiple fault block prospects on the Thali licence, including the existing oil discovery at Njonji in the southern part of the licence, together with their calculated Net Present Value ("NPV") and Expected Monetary Value ("EMV"), as detailed below. The NPVs and EMVs have been calculated based on two price sets: a standard North American forecast methodology using a February 2020 forecast price for 2021 and a constant money price escalation of 2% pa - the "Sproule Energy Forecast" - in order to provide comparability with other reports on other assets using this type of methodology; and the actual Brent Forward Curve at close of business on 10th March 2020, which is the primary focus of this 2020 Reserves Report, to illustrate the impact of the recent fall in oil prices, and to confirm the economic viability of the contingent resources in the current lower price environment.

2020 Reserves Report highlights:

- Gross mean contingent resources of 18 MMbbls of oil across the proven Njonji-1 and Njonji-2 fault blocks (with low/best/high estimates of 5/15/34 MMbbls) are unchanged, with a development contingency probability of 80% on first phase and 70% on second phase;

- Gross mean prospective resources of 20 MMbbls of oil across the Njonji South and Njonji South-West fault blocks (with low/best/high estimates of 5/16/39 MMbbls) are also unchanged;

- Gross mean prospective resources of 111 MMbbls of oil across four identified prospects located in the Dissoni South and Idenao areas in the northern part of the Thali licence (with low/best/high estimates of 21/84/237 MMbbls) are also unchanged;

- The NPV10 of the Best Estimate of Contingent Resources using the Sproule Energy Forecast is $179 million, with an EMV10 of $143 million, however it should be noted that these figures are based on a February 29th forecast based on a 2021 Brent price of $68/barrel;

- The NPV10 of the Best Estimate of Contingent Resources using the March 10th 2020 Brent Forward Curve is $119 million, with an EMV10 of $91 million - these figures compare with the 2018 Reserves Report NPV10 of the Best Estimate of Contingent Resources of $158 million, and an EMV10 of $118 million using the then-current Brent Forward Curve at a time when the 2019 forward Brent price was over $71/bbl.

The reasons why the NPV10 and the EMV10 of the Contingent Resources at Njonji have fallen by less than 25% compared to the figures in the 2018 Reserves Report, despite an approximate halving of the oil price, are that:

- Forward Brent prices have fallen by less than prompt prices, which is usual when the prompt market is oversupplied, so for example the average forward price of Brent in 2021 is approximately $44/barrel;

- The projected costs of the project, which are low, have actually fallen a little reflecting the Company's actual experience in sourcing equipment and services for the NJOM-3 well; and

- The profit allocation mechanism in the PSC attributes a greater share of oil to the contractor when oil prices are low, and a smaller share of oil when prices are high, which can be observed in the different volumes of recoverable oil "attributable to Tower" for the different price scenarios, when comparing the tables below to those in the 2018 Reserves Report.

Jeremy Asher, Chairman and CEO, commented:

"We are pleased to present this updated 2020 Reserves Report on the Thali licence in Cameroon. I already observed last year that our project economics were attractive across a wide range of oil price scenarios, and in September last year I presented one of our internal cash flow forecasts showing the very attractive cash generation from the project assuming a flat $40/bbl Brent price, which can be still be found in our September 2019 corporate presentation on our website. The 2020 Reserves Report confirms the attractiveness of the Njonji project economics.

It is also worth noting that the riskier prospective resources on Thali can be tested at very low cost during the process of developing the contingent resources already discovered. In particular, the Phase 1 development process at Njonji will also test the Njonji South Prospective Resources of 18 million barrels (Pmean), which would be additional to the 18 million barrels (Pmean) of existing contingent resources already discovered at Njonji, thus providing a natural additional upside to the project which is not reflected in the NPVs and EMV10 of the contingent resources.

So even in the lower oil price environment in which we now find ourselves, which echoes the price environment at the end of 2015 shortly after we first entered the Thali license, the Thali license is an attractive asset which we expect will earn excellent returns."