Robert Chambers, Actionable insights and advisory | Upstream and LNG

Global upstream M&A headlines have been dominated by large-scale consolidation in North America, where transactions have focused on efficiency, scale and capital discipline. Against that backdrop, Southeast Asia’s quieter but increasingly dynamic recovery has attracted comparatively less attention.

Pre-COVID Structural Reset

In the years immediately preceding COVID, regional headlines were dominated by the expiry of major PSCs and concessions in Indonesia and Thailand, with operatorship transferring to national oil companies. These structural transfers occurred alongside a broader wave of portfolio rationalisation by international operators, as capital discipline and intensifying energy transition pressures prompted a focus on core hubs and lower-carbon opportunities. The combined effect reinforced domestic control over mature production and strengthened the perception of international retreat from Southeast Asia.

Post-Pandemic Deal Recovery

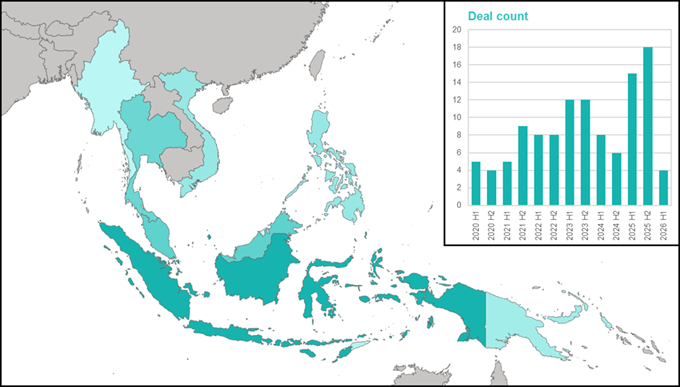

Since 2020, more than 115 upstream transactions have been recorded across Southeast Asia, with deal flow accelerating steadily over the past three to four years. What began as a cautious post-pandemic restart has evolved into sustained transactional momentum, increasingly underpinned by shifting policy priorities and macroeconomic drivers.

Energy Security Reprioritisation

A central policy influence has been the evolution of the regional energy transition agenda. While transition objectives remain embedded in long-term planning, recent geopolitical disruption and LNG market volatility have elevated energy security to a more immediate priority. Governments are increasingly focused on reducing import dependency, sustaining domestic production and accelerating project development. In this context, upstream investment is being framed less as a legacy activity and more as a component of supply resilience — a shift that is influencing not only the volume of transactions, but also their structure and strategic intent.

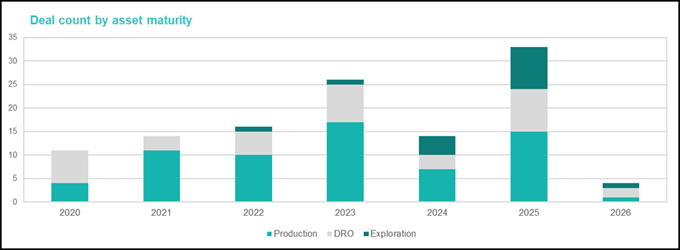

Exploration Returns to the Agenda

Exploration acreage transactions are showing a clear recovery. The absence of exploration-focused deals in 2020 and 2021 underscored the defensive posture adopted during the height of uncertainty, with buyers prioritising producing assets and near-term cash flow. The subsequent re-emergence and steady growth of exploration activity signal a structural shift in capital allocation, with companies increasingly willing to commit to longer-cycle opportunities and future resource capture.

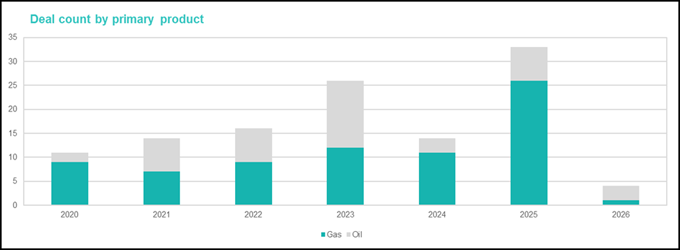

Gas-Weighted Value Allocation

Southeast Asia is structurally gas-weighted, and gas-focused transactions have accounted for an increasing share of activity in recent years, particularly in terms of aggregate deal value, reflecting both domestic supply priorities and LNG-linked development strategies.

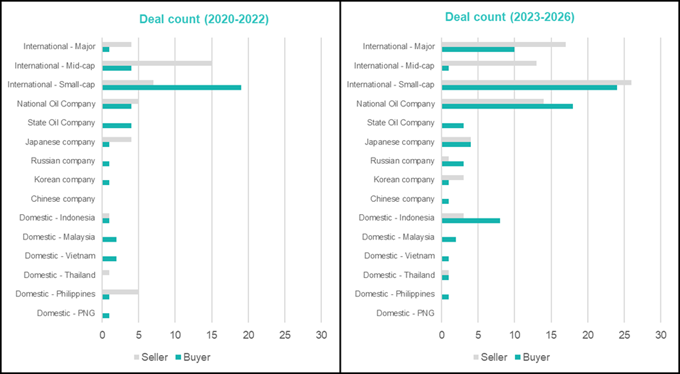

Buyer and Seller Composition

The region presents opportunities across the corporate spectrum, with participation spanning the full range of company types. Analysis of buyer and seller composition reveals a market that is more diverse than often assumed. While majors remain net sellers, they are also selectively expanding — particularly through exploration acreage awards. Meanwhile, small-cap international companies play an outsized role in transaction volume, highlighting the region’s continued accessibility to entrepreneurial capital.

Notably absent as buyers are mid-cap international independents, traditionally active acquirers of maturing assets from IOCs, many of whom have faced tightening access to international bank funding in recent years. In their place, domestic and regional companies such as MedcoEnergi and Hibiscus Petroleum have increasingly assumed this role, consolidating mature production and expanding their regional footprint, with financing frequently sourced from domestic banking institutions.

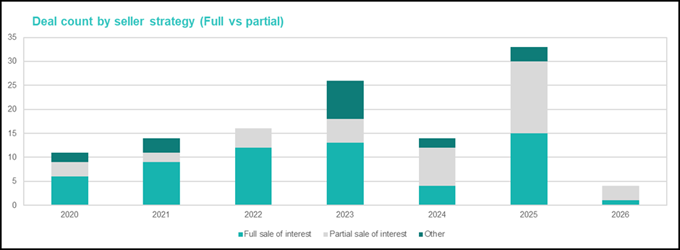

Transaction Structure: Repositioning, Not Exit

Buyer and seller labels alone do not capture the full picture. A closer examination of transaction structure directly challenges the perception of wholesale exit. The early post-COVID years were dominated by full divestments. More recently, partial stake sales have increased materially, suggesting risk-sharing and capital recycling rather than abandonment. In many cases, sellers remain committed operators while bringing in partners to fund development or manage capital intensity.

A Market Repositioned

Taken together, these trends point to a market that has moved beyond a simple post-COVID rebound. Southeast Asia’s upstream M&A landscape is increasingly characterised by ownership rotation, partnership structures and domestic consolidation — underpinned by policy support for energy security. Crucially, this recalibration reflects deliberate repositioning rather than retreat.

Pipeline and Forward Outlook

As we look ahead to the near term, the pipeline of announced and anticipated transactions suggests that this momentum is likely to persist. The region has a number of major ongoing processes that will dominate the headlines:

- The creation of NewCo (now named SEARAH) by Eni / PETRONAS. Public disclosures regarding the number of Indonesian assets and the contributing party provide sufficient clarity to interpret the likely Indonesian asset composition. However, the assets that PETRONAS will contribute from Malaysia remain less clearly defined.

- Related to this, Eni is also selling a minority stake in their Kutei basin assets. Potential interest has been linked to regional NOCs, Japanese and Chinese participants, as well as larger domestic operators and select majors.

- Harbour Energy is reportedly exploring a sale of its Andaman assets, which would mark a regional exit. The potential buyer pool is expected to overlap significantly with participants in the Eni process, with bidder strategy likely shaped by the outcome of that transaction.

- PETRONAS is understood to be evaluating the sale of interests in several key producing assets in Peninsular Malaysia and Sarawak, potentially creating opportunities for smaller operators.

Outside of these headline transactions, there remains significant scope for smaller-scale deals in what appears set to be a sustained period of activity and investment.

KeyFacts Energy Industry Directory: Kawi Energy l KeyFacts Energy: Commentary