By Kathryn Porter

Kemi Badenoch’s proposal to cut energy bills by £200 has been widely dismissed as political posturing, but when looked at properly, from the perspective of consumers and the costs they have to bear, it’s far more coherent than critics would like to admit, and certainly more grounded in economic reality than the current government’s approach to energy policy.

The Conservatives’ plan to cut energy bills explained

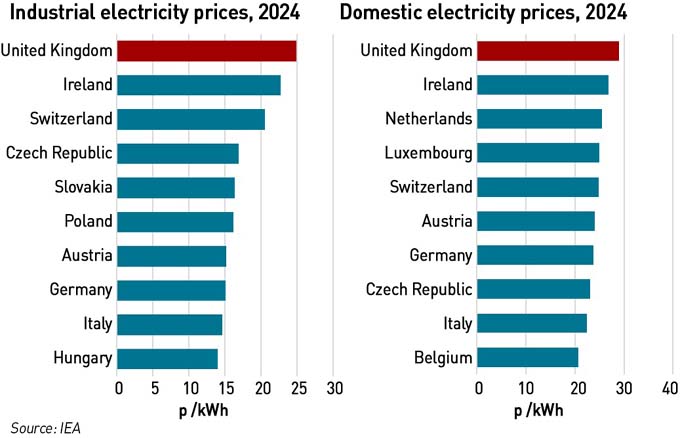

The starting point must be clarity on what households actually pay for, because much of the debate is clouded by metrics that are either irrelevant or actively misleading. There is a huge focus on wholesale prices, with activists and lobbyists posting celebratory commentary about record levels of generation by intermittent renewables, completely ignoring the fact that British consumers are left paying the highest industrial and domestic electricity prices in the developed world.

Consumers do not only pay the wholesale cost, nor do they pay the levelised cost of electricity. They do not pay for individual technologies, and they are not concerned with the internal economics of generators except where those costs are passed through to bills. What households pay for is the cost of running an electricity system so that when they press the light switch the light comes on, regardless of the weather, the time of day, or how many other people are also pressing light switches at the same time. So what consumers have to pay for includes not only the wholesale cost of electricity, but also balancing costs, constraint payments, curtailment, network reinforcement, capacity payments and policy costs, and supplier operating costs and profits. All of these are ultimately borne by consumers either directly through bills or indirectly through taxes.

The components of the proposed £200 are:

- Removing VAT on bills which would save around £94 per year based on current forward price cap expectations

- Removing carbon pricing from electricity generation reduces costs by around £70–75 per household, given the impact of the UK ETS and Carbon Price Support

- The residual cost of the Renewables Obligation (“RO”) about 75% of which was recently moved to taxation. The Conservatives have pledged to scrap this scheme altogether do cutting the cost from bills would be a real saving and not just a change in recovery. This is worth around £20–25 per household

- There is a further plausible saving of around £10 from increased domestic gas production displacing the most expensive marginal LNG cargoes, which would slightly reduce wholesale prices without fundamentally changing the UK’s linkage to TTF

Taken together, those components get very close to £200, and importantly they do so on a consistent basis using the correct metric: total cost to consumers. These are not abstract theoretical savings, but reductions in real costs currently embedded in bills, and while the precise numbers will move with prices, the order of magnitude is sound.

Critics argue that cancelling the RO removes revenue from generators, but that is precisely the point: if a generator cannot operate without ongoing subsidy and at the same time contributes to higher system costs through intermittency, constraint payments and balancing requirements, then its continued operation is not necessarily in the interests of consumers. Without the RO some are likely to close.

You could make a credible argument that this would result in further savings through lower capacity market costs. If some windfarms in the RO close, there would likely be an increase in the use of gas plant. Higher gas utilisation would reduce the “missing money” problem the capacity market was designed to solve.

The debate about costs gets confused because it focuses on the wholesale price and not what the consumer pays. The question isn’t whether gas is cheaper than wind at the station gate, but whether a system with more dispatchable generation and fewer subsidy-driven distortions is cheaper to run. Intermittent generation requires backup capacity, creates additional balancing costs, and drives network investment, all of which add to bills. Indeed the network investment for new renewables is much higher than for an equivalent amount of conventional generation because it has much lower energy density and is often located in areas without existing grid infrastructure.

By contrast, conventional generation avoids many of these costs. A system with more gas generation and less intermittent generation would have lower balancing costs, lower capacity market (backup) costs, lower grid infrastructure costs, lower curtailment costs and of course, lower subsidy costs.

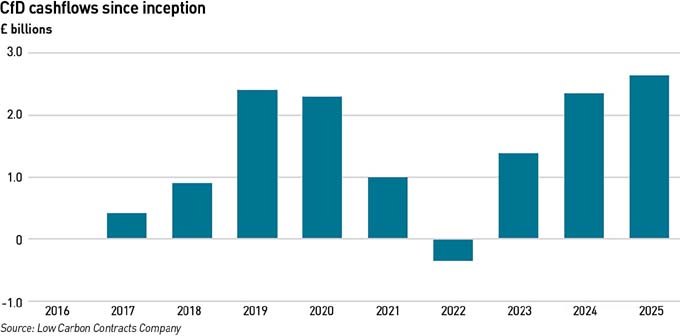

The experience of the 2022 energy crisis illustrates this point. While Contracts for Difference did provide some payback as wholesale prices rose, consumers continued to fund substantial costs through the Renewables Obligation and Feed-in Tariffs, alongside rising balancing, constraint and curtailment costs. The overall benefit of renewables to consumers during the crisis was far more limited than is often claimed.

Even when gas prices fell back to pre-Ukraine war levels, the total system costs remained high. Indeed last October the CEOs of the big energy suppliers gave evidence to the Energy Security and Net Zero Select Committee making many of these points. They made it clear: policy costs and not gas costs are the real problem in the market and the real driver of bills.

“…if we continue on the path that we are on right now, in all likelihood electricity prices for a typical customer are going to be 20% higher in four or five years’ time than they are now. That is even if wholesale prices halve…The point is that the country as a whole at the moment is paying over £20 billion a year on its electricity bills for policy costs. The projections are that that is going to increase. That is one of the hundred pounds that will possibly be added to electricity bills on the current trajectory over the next four years. It is time that we got this burden under control,”

- Rachel Fletcher, Director of Regulation and Economics at Octopus Energy

“We can compare the cost to serve in France and the cost to serve in the UK. Per point of delivery, the cost to serve in the UK is about £100 per annum. In France, it is €45, which is half, more or less. It is actually less than half. This is not to do with the wholesale price or the gas marginal cost et cetera. It is driven by the fact that we have very complex regulation that has become stratified over the years….we have in front of us a system where, even if the wholesale price were to halve, as she indicated, the bills will rise. There are two main drivers that we have in front of us in the growth of the bills. One is the demand reduction. We are building infrastructure as if there was more demand, but, in reality, there is less and less demand, so you have a bigger burden on smaller shoulders…”

- Simone Rossi, CEO at EDF UK

“if I look at the non-commodity costs—policy costs and network costs—certainly some of the modelling that we have suggests that you could get to a position by 2030 where, if the wholesale price was zero, bills would still be the same as they are today because of the increase in those non-commodity costs,”

- Chris Norbury, CEO at E.On UK

“When you look at what consumers pay, consumers do not actually pay the wholesale gas price for anything backed by a CfD. When people talk about getting the wholesale gas price down, that is quite a red herring. Consumers pay what the CfD price is. If the wholesale electricity price goes to a pound, the CfD will simply make that back up to the £75 per megawatt-hour or so that wind farms are getting at the moment,”

- Chris O’Shea, CEO at Centrica

It's also interesting to see these CEOs echoing things you can read on these pages, in my old blogs in the retail market. They describe their activities as “being like a bank” with some suggesting Ofgem may not be the right body to regulate the retail energy market. I have long drawn this parallel arguing for years that retail energy suppliers have more in common with retail banks than other areas of the energy sector and should be regulated as banks, by the FCA / PRA (I would merge those back into a single regulator as in the past – I don’t think the separation has been successful but that’s a topic for another day).

Labour’s economic policies are damaging the UK

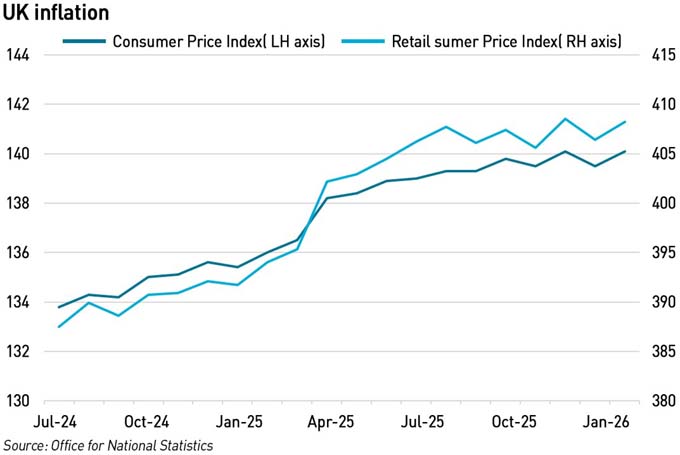

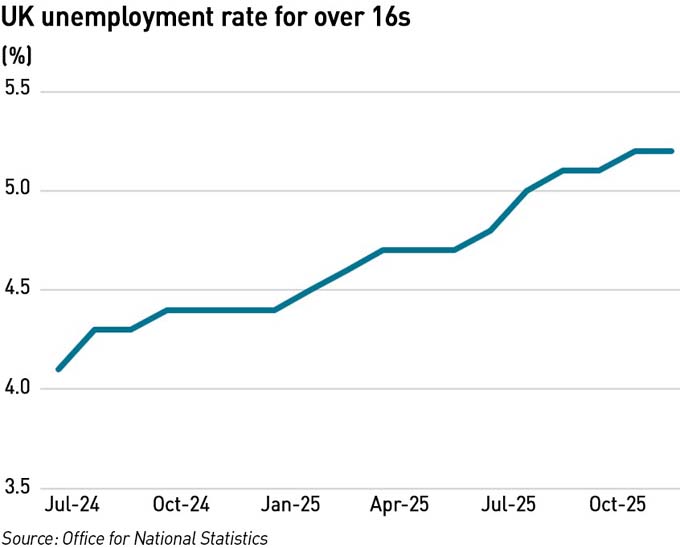

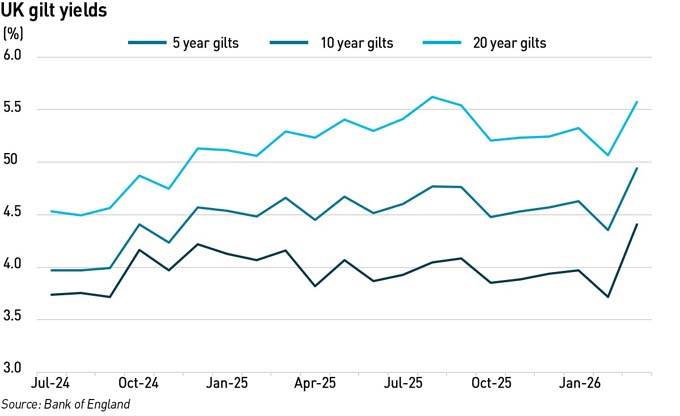

All of this sits within a broader economic context that makes the Government’s current approach increasingly difficult to defend. Inflation remains higher than it was at the time of the General Election, unemployment has risen particularly for young people as plans to equalise the minimum wage deter hiring, and gilt yields - already elevated relative to other G7 economies - have jumped again recently, reflecting persistent concerns about fiscal credibility. These are not marginal changes - for the most part they are significant increases.

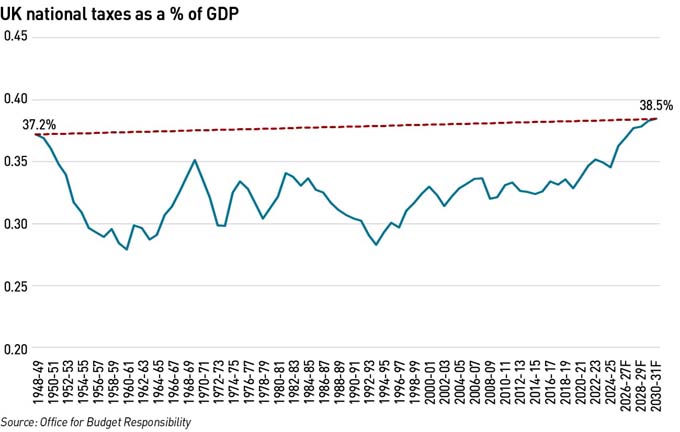

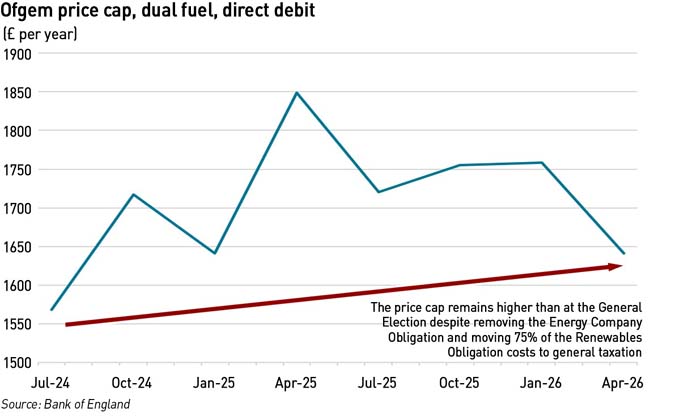

Energy bills were rising again even before the escalation of tensions in Iran. Despite removing the Energy Company Obligation and moving 75% of the Renewables Obligation costs to general taxation, the price cap is still higher than at the last General Election. This has added to £7-8 billion to taxation, despite the UK already having the highest tax burden since the 1940s, at a time when business closures are running at historically high levels. The UK now pays out more in welfare (£333 billion) than it receives in income taxes (£331 billion).

What’s striking is not just the deterioration in these indicators, but the Government’s apparent unwillingness to engage with those raising concerns. Business leaders have repeatedly warned about the direction of policy, with figures such as Jim Ratcliffe criticising the lack of engagement on North Sea policy and broader concerns being raised about the impact of fiscal measures introduced by the Chancellor.

At the same time, ministers have escalated anti-business rhetoric. Within two weeks of the start of Operation Epic Fury in Iran, and one day after tensions in the region escalated significantly, UK ministers began telling the media they would not tolerate “profiteering” by fuel retailers. Given the well-established lag between wholesale price movements and retail fuel pricing, it's difficult to see how robust evidence of such behaviour could have been available in such a short timeframe.

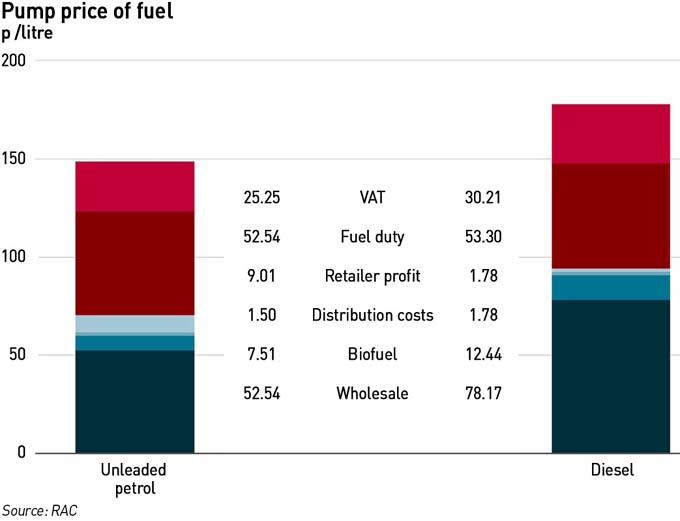

This looks like a political smokescreen to distract from criticism of the Government's approach to the war and deteriorating relations with one of the UK's most important allies, the US. However, the move backfired as it served to draw attention to the huge amount of tax levied on fuel, with more than half of the pump price (at the time, unleaded was just under 150p /litre) being tax, and the fact that VAT is levied on the fuel duty, creating a double tax.

Petrol station operators reported increased aggression towards staff as customers respond to the Government’s unfounded allegations.

Many of the problems now being blamed on external shocks were already evident well before the latest geopolitical developments. Back in January last year, financial journalist Matthew Lynn wrote in Moneyweek:

“The UK has become a very unattractive market for global businesses. Growth has ground to a halt and is now, when measured on a per capita basis, falling. Inflation remains above the Bank of England’s target rate and may well start to rise again over the next few months. The planning system strangles any form of new development and makes it virtually impossible for companies to expand. Even if the government does finally back a few infrastructure projects, such as the third runway at Heathrow, those are decisions that should have been made 20 years ago. The net-zero targets are the most demanding in the world, and industrial electricity is now the most expensive anywhere, imposing huge costs on businesses. The flexible labour market that used to be one of the UK’s strengths compared with the rest of Europe has long since been replaced with some of the strictest employment laws in the world, making it virtually impossible to fire staff who are not performing. And, on top of all that, the UK has left the EU’s single market while doing virtually nothing to compensate by deregulating its own markets.

Even worse, although it keeps talking about growth, the Labour government is hostile to business. In her first Budget, chancellor Rachel Reeves imposed a huge £25 billion tax rise on companies in the form of an increase in National Insurance; clamped down on non-doms, many of whom were investing in companies in the UK; imposed inheritance tax at 40% on people leaving a family business to their heirs, meaning in practice that it would almost certainly have to be sold; and introduced extra windfall taxes on the few companies that by some miracle do manage to make money. If the Budget had been specifically designed to drive out entrepreneurs and investors, it could hardly have done a better job. More tax rises are likely in the year ahead, given disappointing growth, and the insatiable spending demand of the UK’s health and welfare systems, and the burden of the rises will almost certainly fall on businesses.”

Matters have not improved since.

But the UK is not without alternatives. Other countries are beginning to adjust their approach in response to economic pressures. In Germany, ministers have openly acknowledged that net-zero targets may need to be softened to reflect industrial realities. They are also considering firing up coal plants to mitigate rising energy costs as a result of the war in Iran. In Italy, Giorgia Meloni has called for changes to European carbon markets, including suspension of the ETS, and there have been discussions at the Commission level about increasing the supply of permits to reduce energy costs for industry. These are pragmatic responses to changing conditions, recognising that policy must adapt if it is to remain economically sustainable.

By contrast, the UK government appears determined to hold its course regardless of the consequences amid what can only be described as hostility and suspicion towards business. Plans to increase rather than reduce fuel duty, reluctance to provide meaningful support to domestic refining through mechanisms such as the Carbon Border Adjustment Mechanism, and the continued refusal to lift the Energy Profits Levy or the effective ban on new North Sea drilling all point in the same direction within the energy sector.

Elsewhere, new employment laws have just come into effect, after businesses were slammed by higher taxes last year. Everyone except the Labour Party seems to recognise that this will further threaten jobs and the employment prospects of young people, which have already taken a turn for the worse. The CBI annual CBI/Pertemps Employment Trends Survey last September found that 86% of respondents believe the UK labour market is a less attractive place to invest and do business compared to five years ago, with 54% ranking it as much less attractive. 82% expected this trend to continue, with labour costs ranking as the top threat to labour market competitiveness for 73% of respondents. The impact of employment regulation on flexibility ranked second (65%) followed by access to skills (58%).

This came after the UK’s five largest business groups, including the CBI, warned last April that the government’s flagship workers’ rights package would be “deeply damaging” to the UK’s growth prospects and will worsen living standards in the UK. They said:

“Our collective position is that… the Bill will have deeply damaging implications for the government’s priority growth mission as well as their admirable focus on tackling rising economic inactivity,” the group of industry bodies warned, saying that “taken together, [the policies are] a recipe for damaging, not raising living standards.”

Just last week a consortium of trade bodies in the catering sector said that despite business rates support for pubs, “neighbourhood restaurants, local hotels and independent cafés all face their bills rising in the thousands”, and that from this month when new rules come into force, they are “facing billions of pounds in additional costs, which will force many to make heartbreaking decisions”.

A recent survey from UKHospitality, the British Beer & Pub Association, the British Institute of Innkeeping and Hospitality Ulster has found that, as a direct result of cost increases, 64% of hospitality operators will cut jobs, half will cancel investment plans, just over 42% will reduce trading hours, and 15% of venues will be forced to close. A survey by the Federation of Small Businesses found that 92% of small employers are worried about the Employment Rights Bill, with 67% saying they plan to recruit fewer staff, and 32% planning to reduce headcount.

Labour’s economic and regulatory changes are hammering farming, hospitality, retail and energy-intensive industries such as refining. Logistics, social care, construction, leisure and tourism are all also suffering while the Government turns a deaf ear. The CBI says its concerns have been “largely ignored”, a view shared by the Institute of Directors.

“A perfect storm of government policies via the Employment Rights Bill, above-inflation increases to the National living Wage, and the increase in Employer National Insurance Contributions have significantly weakened the business case for hiring staff. An IoD survey of over 600 business leaders last month found employment regulation is the biggest regulatory blocker to business growth in the UK, with 45% citing it as a barrier to their company growing. At the same time, six in 10 cited employment taxes as negatively affecting their organisation. The government’s refusal to engage with sensible amendments made to the Employment Rights Bill in the House of Lords is sending a clear signal to businesses that their concerns are being ignored.”

- Alex Hall-Chen, Principal Policy Advisor for Employment at the Institute of Directors

The British Chamber of Commerce says that consultation on the secondary legislation which will govern many of the day-to-day practicalities of the Employment Rights Act will be vital: “businesses are clear they still have major concerns about the workability and costs of several other powers in the Bill”.

Unfortunately, this Government lacks any prominent members who have any experience with running a business, while energy policy is run by an ideologue who has built a reputation in the industry for refusing to engage with anyone who does not share his ideology. As a result, there is a deep reluctance to take the concerns expressed by businesses at face value. The Government repeatedly says it wants economic growth and that this is a “priority”, but it then uses its huge Parliamentary majority to force through fiscal and regulatory changes that have the exact opposite effect. This is already visible in the data.

Rather than responding to economic reality, policy is being driven by a fixed view of what the system should look like, even as the costs (and risks) of that approach become increasingly clear. The result is a growing disconnect between policy and outcomes. The UK is not helpless in the face of global energy markets or economic headwinds, nor is it inevitable that consumers must bear ever-rising costs.

There are choices available, but they require the Government to listen to a wider set of views with a more open mind than it has to date. And to be willing to compromise. Almost two years into this Parliament, it should be clear that important economic indicators are going the wrong way, and that perhaps academic theories of growth are not a substitute for real-world experience.

A focus on total system cost – not just in the energy sector, but across the economy as a whole - would be a good place to start.

Original article l KeyFacts Energy Industry Directory: Watt-Logic