By Jenna Harris

Over the past decade Sasol has been properly taking a beating. Its no secret that their US Lake Charles chemical project turned from what should have been a boon into a major bust. Massive overspend coupled with one of the biggest chemical commodities price slumps left Sasol with a debt burden so large it threatened to tank the company.

Next problem: Despite an apparent additional 50 year coal reserve supplying Secunda, the stuff coming out the ground was getting harder to get out and started looking less like coal. This pushed up input costs and lead Sasol to start scrambling for externally sourced coal supply.

Next problem: Oil prices stagnating. Noting that Sasol's fuels are sold at "Import Parity" prices - ie: price matching to what it would cost to import the same fuels, stagnating oil prices and increasing input costs were leading to a rather uncomfortable margin squeeze. And that margin was being used to service the newly inflated debt burden - ouch.

Next problem: 2019 Sasol makes their SEC 19F filing flagging a forecasted decline in their Mozambique gas supply from 2024. Sasol's gas supply not only is used internally, but also supplies the market - putting Sasol's long term gas business under threat. As of yet, Sasol has not been able to source a real alternative gas supply despite the past decade's search.

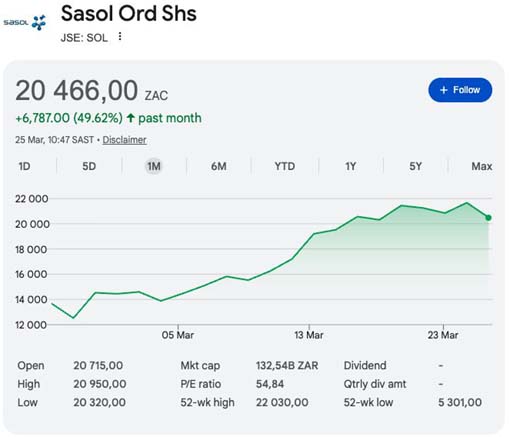

The past month has been a massive shift - the war in the middle east has spiked up both oil prices and crack spreads...and in turn, Sasol's product prices. In the same period, Sasol announced their new coal de-stoning facility to be commissioned, meaning better efficiencies and decreased input costs. A BIG win for Sasol, with the convergence of these factors bringing more cash to the bank. The longer the Strait stays closed, the more war chest Sasol can build up (no pun intended)!

What we don't know however, is the current status on Sasol's Gas to Liquid facility in Qatar (Oryx GtL). Oryx sits in the Ras Laffan Industrial City, the same mega LNG industrial complex which has been directly affected by the conflict and exports through the Strait of Hormuz. Although there are no confirmed reports, one can reasonably assume its exports have been disrupted.

That being said, ORYX looks bigger on paper than it does in cash — the actual dividends upstreamed to Sasol are relatively small in the context of the group.

All in all, the markets have taken an overall positive sentiment in Sasol's share price - up about 50% over the past month!

Is this the turning point Sasol has been waiting for — or the moment the market finally starts pricing in the strategic value of energy security?

Jenna Harris is a seasoned energy executive and entrepreneur with over two decades of experience spanning power generation, regulatory reform, and market creation across Africa and Australia.

KeyFacts Energy: Sasol South Africa country profile