By Kathryn Porter

The Capacity Market was introduced with a very clear and sensible objective - to ensure that Britain would always have enough firm capacity available to meet demand, even under stress conditions (particularly periods of low renewables output) by providing revenue certainty that would support both new investment and the retention of existing generating plant.

Essentially, it’s an insurance mechanism for the electricity system, and like any insurance policy, its value lies not in normal conditions, but in the extremes: those cold, still winter periods when demand is high, renewable output is low, and the system is under genuine strain. The problem is that the way the market is now being run looks more like a cost-optimisation exercise built around optimistic assumptions and a bias in favour of supporting official policy narratives, rather than a robust assessment of worst-case system needs. The latest T-4 auction suggests that this gap between theory and reality is widening.

The capacity market design no longer matches physical reality…

At the heart of the design is the distinction between the T-4 and T-1 auctions, with the former intended to secure the bulk of capacity four years ahead of delivery and the latter acting as a relatively minor top-up mechanism closer to real time. The choice of a four-year horizon reflected the typical real-world construction period for new gas-fired generation at the time the market was created. A CCGT can be built in about 18 months from breaking ground to commissioning, with additional time built in for permitting, securing supply chains, and other practical scenarios that mean the plant is rarely built in line with the fastest possible timetable.

The T-4 auction is not just a procurement exercise, but an investment signal indicating the need for new capacity. Indeed, the market was created with an intention to secure new large gas generators – it has completely failed to do this (the only newbuild CCGT - Carrington - delivered to date with a capacity contract took FID before it even entered the capacity auction, so was not dependent on securing a contract).

However, the four-year structure also means that any errors in the assumptions underpinning the T-4 procurement target are locked in for the medium term, because the system has very limited ability to correct for them later, and certainly not at scale. The T-1 auction cannot compensate for a shortfall of several gigawatts of firm capacity; it can only fine-tune around the edges.

This makes the choice of procurement target critically important, and it is here that the recent auction raises serious questions.

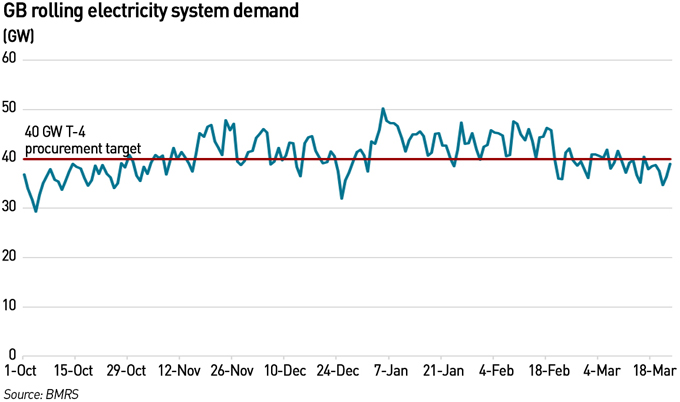

The most recent T-4 auction procured just over 40 GW of capacity against a target of 39.4 GW, with around 44 GW entering the auction at the pre-qualification stage. Yet typical weekday peak demand this past winter was around 45 GW, with the highest transmission system demand seen in Winter 2025/26 of just over 50 GW. A 40 GW T-4 target doesn’t even secure typical daily peak winter demand, never mind the expected demand in a period of system stress. With the actual transmission system peak demand this winter over 50 GW, why was that not the auction target?

Of course, only 44 GW entered the auction, but it’s entirely possible for the capacity market to procure the entire pre-qualified stack – effectively, there is no auction and capacity is awarded at the price cap (the reserve or “maximum clearing price”). This has happened before. At least this would have mostly covered the typical weekday peak.

But even 44 GW is completely inadequate. Not only does it fail to cover the actual peak demand, but it assumes there is no electrification. NESO’s Clean Power 2030 analysis assumes electrification will add around 11% to electricity by 2030 based on the 2023 peak demand (for the total system, not just the transmission system) of 58 GW, i.e., an increase of over 6 GW, and data centres another 6 GW based on Government projections. So in 2030, NESO and DESNZ think peak demand will be 70 GW. So why are they only procuring 40 GW of capacity in the capacity auction for 2029/30?

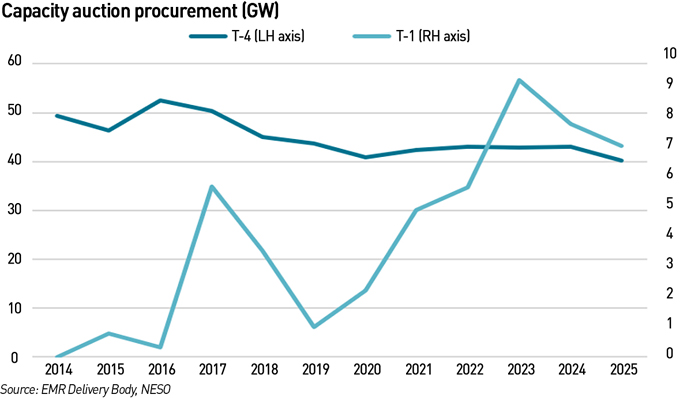

In fact, the capacity being secured in the T-4 auctions is falling. This implies that, despite the projections around electrification, the Government and NESO think demand is going to fall. This is consistent with what has been observed on the grid as deindustrialisation has been the dominant demand driver ahead of electrification, but it is not what policy is trying to achieve. Nor is it necessarily credible that we will see demand destruction on this scale.

Or they are assuming renewables will make up the 30 GW difference. But that logic would undermine the very purpose of the capacity market….the whole point of the mechanism is to ensure system adequacy during periods when renewable output is minimal – those cold, still winter days when demand is high, and wind output is low (and there is zero solar in the evening peak as it’s after sunset). If the system is assuming tens of GW of renewable output in those periods, then it’s effectively contradicting its own founding assumptions of ensuring there is enough generation available to cover periods of low renewables output.

Alongside this sits further uncertainty in the form of construction and delivery risk associated with new build and refurbished assets that have secured contracts but are not yet operational. The four-year lead time of the T-4 auction is intended to mitigate this, but in recent years, supply chains have extended. The lead time for a new gas turbine is now 7-8 years, meaning a developer would need to bet 3 years ahead of any auction that it would secure a contract. There is no evidence that this is happening, which is not surprising, since any new large gas generator would need the certainty of a capacity contract to secure the financing it would need to go ahead with its project, and it’s unlikely to place (or have accepted) an order for expensive equipment on a speculative basis.

The situation with Drax further underlines the risks developers take – it built 3 OCGTs in time for the start of their capacity contracts in October 2024. However, only one has opened, having recently been commissioned, because the grid connections weren’t built in time. Despite having zero control over this, developers face the full risk of delivery. Unless you’re a wind farm, where Connect & Manage allows wind farms to be built despite knowing most of their output cannot be used. For example, Seagreen, which opened in October 2023, in 2024 67% of its output was curtailed, rising to 75% in 2025. A total waste of consumers’ money.

The market needs to be redesigned to take account of longer lead times for key equipment and potential delays to grid connections, bringing better alignment and ensuring developers of dispatchable generation are not exposed to unreasonable levels of risk. And procurement targets need to be realistic.

…and the wrong type of capacity is being procured

The composition of the capacity that has been procured compounds these concerns, because a growing share of it is not firm in any meaningful sense, even if it is treated as such within the market design. In particular, the increasing reliance on interconnectors and unproven demand-side response introduces a degree of conditionality that flies in the face of what the market is intended to achieve.

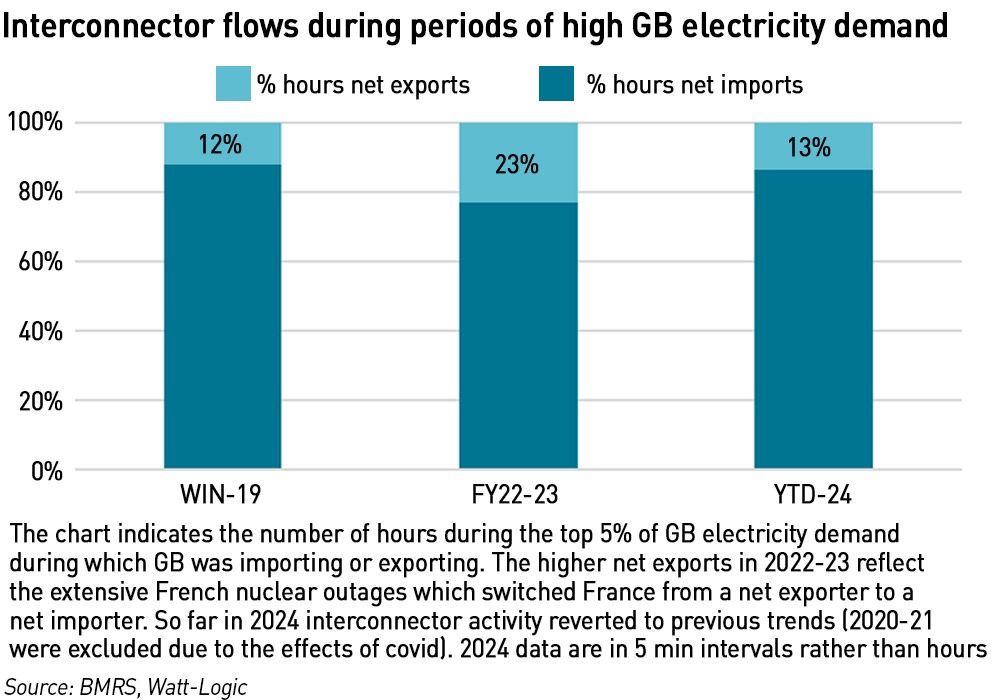

Interconnectors are generally counted as being equivalent to domestic generation, but they are fundamentally different: they do not create energy; they simply allow it to flow between markets. In a stress event, the UK can restrict exports, but it cannot compel imports, and if neighbouring markets are themselves tight, which is entirely possible given the high weather correlation with most of these markets, then the assumption that interconnectors will deliver power into Britain becomes highly questionable.

In fact, my previous analysis shows that at times of high demand in GB, we’re often exporting. France has a more weather-sensitive electricity system than we do since electric heating is more widespread, so when temperatures fall, electricity demand rises faster than in Britain, where gas dominates heating.

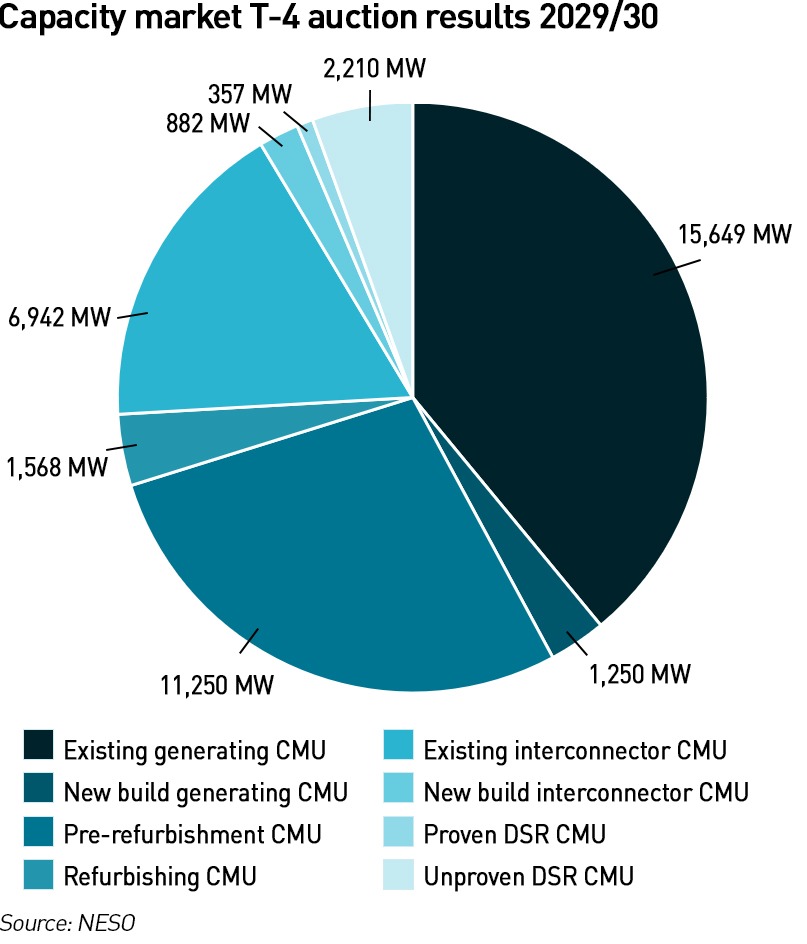

Yet interconnectors accounted for 20% of the capacity awarded in the most recent T-4 auction.

Unproven demand-side response raises a different set of issues, but creates a similar lack of certainty. These resources are, by definition, not yet demonstrated at scale under real system stress, and often rely on behavioural assumptions about how consumers or businesses will respond when called upon to reduce demand. While there is clearly some value in demand flexibility, particularly for short-term balancing, it’s much less clear that it can be relied upon to deliver sustained reductions during prolonged stress events, particularly as those events can coincide with periods of high economic activity or extreme weather.

Treating such resources as fully equivalent (on a de-rated basis) to dispatchable generation risks overstating the amount of genuinely deliverable capacity on the system, and the more heavily the market leans on them, the greater that risk becomes.

Unproven DSR secured 5% of the capacity in the latest T-4 auction, far more than the 1% secured by proven DSR (2,210 MW versus 357 MW), indicating that the market is increasingly favouring lower-cost, higher-risk capacity over demonstrably deliverable capacity. This is a real problem - unproven DSR has secured a non-trivial share (5%) of total capacity, despite having no operational track record, while proven DSR, which has demonstrated delivery capability, accounts for much less of the total capacity awarded.

The capacity market is a price-clearing auction where lower-cost resources are naturally favoured. Unproven DSR can bid at lower prices because it has lower capital requirements and less exposure to construction risk. But that doesn’t make it lower risk from a system perspective - on the contrary, it shifts risk from investors to the system operator, and ultimately to consumers, because the penalty for non-delivery is not necessarily high enough to guarantee performance in a genuine stress event.

Together with interconnectors, highly uncertain technologies account for a quarter of the capacity awarded. This is a huge proportion, particularly when the low procurement total is taken into account. This can result in a system that is not only tighter than it appears, but also increasingly dependent on capacity that simply might not materialise when it’s needed most.

What emerges from all of this is a system that appears adequately supplied on paper, but is significantly more constrained in reality, particularly under stress conditions. A procurement target that is too low, combined with a growing reliance on capacity that’s either conditional, not under our control, or not yet built (and may not be capable of being built or connected in the available time), creates a false sense of security over actual system adequacy. This is not an abstract concern, but a structural issue in how security of supply is being assessed and delivered.

A more robust approach would start from the recognition that the purpose of the capacity market is not to minimise costs in the central case, but to ensure reliability in the tail of the distribution, where the consequences of failure are greatest. That would imply a higher procurement target, more closely aligned with historical peak demand and forward-looking estimates of growth, as well as a much more conservative treatment of interconnectors and unproven demand-side response. It would require a clearer focus on securing genuinely firm, dispatchable capacity, even if that comes at a higher upfront cost.

And the market needs to take into account of actual real-world delivery timetables. If supply chains have lengthened, the auctions must be held earlier than 4 years ahead of delivery so that developers are not excluded by an expectation that they would not be able to deliver on time and would incur penalties.

The capacity market was introduced to ensure that firm generating capacity did not leave the market when utilisation rates were pushed down by renewables, so they would be available to run on low wind, low sun days, and that new firm capacity would be built to cover increased demand from electrification or retirement of ageing plant.

But there seems to be a growing reluctance to properly pay for this, fudging the issue with interconnectors and unproven DSR, which is cheaper to procure but may well not deliver. Capacity that might not deliver in a system stress event has no place in a capacity market.

And setting procurement targets far below any realistic view of actual demand in a system stress scenario makes even less sense. This market will get tested at some point and is likely to be found lacking. The Iberian blackout taught us that lives are at risk when system adequacy is compromised, and the economic costs are significant, so this should not be taken lightly.

NESO and DESNZ need to explain why the procurement target is so low compared with actual realised demand and their own demand growth targets. They need to re-evaluate the reliance on uncertain and unproven technologies, and they need to better align the timetable with real-world supply chain constraints. And Ofgem needs to ensure that the market is being run in a prudent way, avoiding undue complacency.

KeyFacts Energy Industry Directory: Watt-Logic