WTI (May) $94.48 +$4.16, Brent (May) $108.01 +$5.79, Diff -$13.53 +$1.63

USNG (Apr) $3.00 +5c, UKNG (Apr) 140.50p +5.97p, TTF (Apr) €56.20 +€2.075

Oil price

Oil has rallied again today, a bit like yesterday when markets have conflicting views as to the direction of travel. As I write WTI is $97.10 and Brent $111. President Trump has said that the ceasefire from the US side will go on for another 10 days or at least until April 6th.

Arrow Exploration

I was very fortunate to be able to interview Marshall Abbott, CEO of Arrow Exploration this week and the almost unexpurgated version is in the link below.

In our discussion we had a detailed review of the significant progress that has been made at the Mateguafa attic play in recent months. Marshall gave me plenty of information about the wells that have been drilled and why the Icaco exploration well will be drilled after the current M-12 horizontal well is completed.

Whilst the rest of the portfolio is still in incredible shape the fact that the ‘attic’ has performed so well is a real boost to both reserves and production, also the company has drilled some of the longest ever horizontals in country and resolved significant technical issues.

With construction of more cellars at Mateguafa, in preparation for another campaign and also for the M-8 to become a water disposal well, Arrow are growing the scope of the play and adding to its knowledge of the formations therein.

We also talked about current production which is c.5.4m b/d and with more potential from the Mateguafa and also Icaco, short term is excellent and longer term growth looks solid, the 10/- b/d target remains in the company’s mind.

I remain confident that Arrow has a very bright future, my 40p target price is very achievable and its place in the Bucket List is assured given how good the prospects are.

Core Finance CEO interview: Marshall Abbott of Arrow Exploration

Jadestone Energy

Jadestone yesterday announced that it has successfully completed a US$200 million senior secured bond issue with maturity in 2031 and a coupon of 12%.

The bond placement was materially oversubscribed and saw strong investor demand across Nordic and international markets. The Company’s largest shareholder, Tyrus Capital, subscribed for and was allocated US$25 million in the bond issue. The bond principal amortizes at US$50 million per annum from the third anniversary of the bond issue with a final repayment of US$100 million at the maturity date.

For the purposes of AIM Rule 13, the participation by Tyrus Capital in the Nordic Bond Issue constitutes a related party transaction. The Independent Directors (being directors who did not, together with their affiliates, participate in the Nordic Bond Issue), having consulted with the Company’s nominated adviser, consider that the terms of this related party transaction are fair and reasonable insofar as its shareholders are concerned.

Dr. Adel Chaouch, Executive Chairman, commented:

“We are pleased that our debut bond offering generated substantial demand from credit investors seeking exposure to the strong upstream growth story of the Asia-Pacific region. The Nordic Bond Issue will deliver a strong financial foundation for the business, and allow Jadestone to focus its near-term cash flow generation on growth opportunities, particularly as we seek to move our Vietnam development forward following the key recent milestone of field development plan approval.”

This was a highly successful visit to the bond investors for Jadestone, only a week after having announcing the meetings they have delivered a ‘materially oversubscribed’ placement. In less than a week they have completed marketing, bookbuilding and placement in what must have been considered to be a somewhat difficult market.

The institutional demand was strong and buyers seen across a number of different regions but the uniting factor was the desire for investors to gain exposure to the fast-growing energy markets of Asia-Pacific.

As noted last week, refinancing the RBL allows Jadestone to keep more cash flow generation in-house which can be spent on growth, in particular following the key milestone last week of the FDP approval for the Vietnam project as well as other inorganic opportunities.

Jadestone is looking better day by day, good news on the asset front and also on the balance sheet will lead to faster, more efficient development of what is a rapidly improving portfolio and with that ongoing demand from the Asian Pacific markets the company is very well placed.

The shares have been performing well, my target price of 75p is looking achievable and its place in the Bucket List assured, I am confident that the outlook is very promising.

Prospex Energy

Yesterday I was on the Prospex Investor presentation which was an important opportunity for new CEO Tom Reynolds to share his views and to elucidate his plans outlined in his recent letter to shareholders.

To me the presentation hit just the right tone, Reynolds went through the portfolio in great detail and not sugar coating anything, where cash would be needed and also how he can get the best from each asset individually.

The result was that he sees a really good bunch of assets which have varying time scales in terms of return but nevertheless is a really good portfolio. The Poland acreage is just coming in and adds to the way the assets are balanced, I liked the slide which showed the potential upside and it looks like he has joined at a good time.

Finally he has made it perfectly clear since he started that he is not keen on equity raises per se, but that other, left field ways of financing will be considered especially if it can avoid dilution which will enamour him to shareholders.

All looks good here and what I probably liked best is that Tom has made it clear that his remuneration is subject to shareholders winning first. I see plenty of upside, the market for European gas is strong and only getting stronger and with the under new management sign well and truly up things can only get better…

Prospex yesterday announced the release of its latest corporate presentation, which Tom Reynolds, CEO, will be presenting at the Investor Meet Company Event this afternoon, 26 March 2026, at 3:00 p.m. The presentation is available on the Company’s website: www.prospex.energy.

This event is a prime opportunity for existing and potential investors to gain valuable insights into Prospex Energy’s growth strategy, operational progress and the expanding opportunities in the European energy market.

The presentation contains an update on the Company’s investment strategy and certain assets, including:

Viura, Rioja Province, Spain

- Average production rates during January and February 2026 are 101,000 Ncm/d gas and 148 cubic metres produced water per day

- These rates are not indicative of steady state operation as the operating regimes have been selected to inform boundary conditions within the dynamic model

- The Company expects the modelling work to have completed by end April 2026 and a steady state operational regime established

San & Dunajec exploration licences, Poland

The Dunajec licence contains an undeveloped oil discovery drilled in 1966 which may contain up to 2 million barrels Oil Originally in Place based on historic estimates with 13m of pay interval measured in fractured carbonate at a depth of c. 600m.

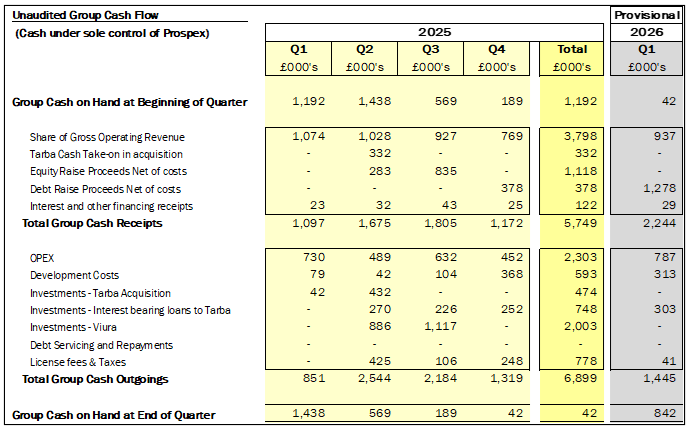

2025 Cash Reconciliation

The presentation includes an unaudited cash reconciliation for calendar year 2025 and an indicative estimate for Q1 2026 which takes account of cash directly controlled by the Company but excludes cash flows related to its 7.5% ownership stake in HEYCO Energy Iberia corresponding to the Viura field.

This announcement contains inside information for the purposes of Article 7 of the Market Abuse Regulation (EU) 596/2014 as it forms part of UK domestic law by virtue of the European Union (Withdrawal) Act 2018 (“MAR”) and is disclosed in accordance with the Company’s obligations under Article 17 of MAR.

Seascape Energy Asia

Seascape has confirmed, further to the announcements made on 24 and 25 March 2026, the result of its Fundraise and Retail Offer at the Issue Price of 70 pence per share. The Company announces that the Retail Offer was several times oversubscribed, and it has raised aggregate gross proceeds of approximately £840 thousand pursuant to the WRAP Retail Offer, alongside the previously announced Placing and Subscription. Accordingly, the Company will issue a total of 1,200,000 new Ordinary Shares at the Issue Price pursuant to the WRAP Retail Offer.

In total, the Placing and Subscription and the WRAP Retail Offer have raised gross proceeds of approximately £5 million for the Company, via the Placing and Subscription of 6,000,000 Placing and Subscription Shares and the 1,200,000 WRAP Retail Offer Shares.

A good result all round as the retail offer was 3x oversubscribed with all getting something from it and the company raised £5m. The shares are unchanged today so everyone should be happy, all in all a good job in difficult markets.

Chariot

Chariot has confirmed that further to the Company’s announcement on 19 February 2026, a subsidiary of Etu Energias S.A has signed a sale and purchase agreement to acquire a 20% working interest in Block 14 and a 10% working interest in Block 14K, offshore Angola. Etu Energias S.A is a 100% Angolan-owned exploration and production company.

- Chariot has part financed this Acquisition through providing deposit funds of US$12m and additional financing related transaction costs (the “Chariot Funds”) and in doing so has secured exposure to the economics associated with material oil production following completion of the Acquisition

- Shell Western Supply and Trading Ltd (“Shell Trading”) has provided an acquisition financing package (“the Shell Facilities”) in return for future offtake barrels. These facilities will be used to finance the final consideration payable on completion, which will be reduced by interim period adjustments

- This funding combination ensures that the Acquisition is fully financed and the Chariot Funds will be repayable from future cashflows from the asset, after servicing the Shell Facilities

- In addition, Chariot will be economically exposed to long-term future cashflows equivalent to current production of circa 4,000 bopd and an equivalent indicative asset value of net NPV10 in excess of US$100 million at a US$60/bbl oil price

- Completion of the Acquisition is subject to regulatory approvals with closing expected in H2 2026

Adonis Pouroulis, CEO of Chariot commented:

“This is a key step in the transaction process for our Angolan partners, Etu Energias. We are delighted to have raised the funds and to be able to support them in this acquisition, alongside the significant financing support from Shell Trading. We look forward to completion later this year and working alongside both parties going forward. This is a new chapter for Chariot as we now have economic exposure to material production in one of the best oil provinces in the world. With the future cashflows this deal brings, we are putting valuable oil barrel income on the book and we look forward to growing this out from here.”

Completion of this transaction is excellent news for Chariot and as I wrote in detail when it was announced it is a real game-changer for Chariot as it brings massive scale for the company in what is rapidly becoming one of the best post codes in international energy.

As Chariot moves ahead with its plans to return to being a leading oil and gas E&P player I expect more deals like this, it now has top drawer partners and is strongly financed, welcome home boys.

Europa Oil & Gas

Europa has announced, further to its announcement of 30 January 2026, that it has received notification from the Irish Government’s Department of Climate, Energy and the Environment that the Minister has given his consent to extend the Phase 1 of FEL 4/19 to 31 January 2028. The Company intends to use the extension to carry out further technical studies and allow more time to secure a partner to advance development of the licence.

William Holland, Chief Executive Officer of Europa, said:

“I am delighted that our application has been granted and that we can continue with further technical studies of the licence and seeking a project partner. FEL 4/19 contains the large 1.5 TCF, low risk Inishkea West gas prospect which is a strategic asset that can potentially provide a reliable source of low emission energy for Ireland and play a key role in the transition to renewable green power. Given the proximity to existing infrastructure, a discovery at Inishkea West could be brought online quickly and would reduce Ireland’s reliance on imported gas. Domestic gas from Inishkea West would have significantly lower carbon emissions than imported gas from the UK, Norway or further afield. We look forward to working constructively with DECC as we seek to progress FEL 4/19 to drilling, and to attract additional partners to this prospective licence.”

This is good news for EOG and the shares have responded accordingly, up 8% the last time I looked. It doesn’t need me to tell you that this licence would be a no-brainer for Ireland and whatever the net zero aspirations of the Government nothing works if the lights go out.

Original article l KeyFacts Energy Industry Directory: Malcy's Blog