Introduction

Carbon capture, utilisation and storage (CCUS) has emerged as a critical component of the United Kingdom’s strategy to achieve net-zero greenhouse gas emissions by 2050. The technology involves capturing carbon dioxide (CO₂) emissions from industrial processes or power generation, transporting the CO₂ via pipelines or ships, and storing it permanently in geological formations such as depleted oil and gas reservoirs or deep saline aquifers. In some cases, captured CO₂ can also be reused in industrial applications, a process known as utilisation.

The UK is widely considered one of Europe’s leading markets for CCUS development due to its favourable geology, existing offshore oil and gas infrastructure, and strong policy support. The government has positioned CCUS as a cornerstone of its energy transition strategy, particularly for decarbonising “hard-to-abate” industries such as cement, refining, chemicals and steel production. These sectors generate substantial emissions that cannot easily be eliminated through electrification alone.

Policy support for CCUS has accelerated significantly over the past decade. The government has committed tens of billions of pounds to the development of carbon capture clusters and associated infrastructure. These clusters aim to connect multiple industrial emitters to shared CO₂ transport and storage systems, creating economies of scale and reducing costs. The ambition is to establish the UK as a global leader in carbon capture while supporting regional economic development and preserving industrial competitiveness.

This report examines the current state of carbon capture activity in the United Kingdom. It reviews government policy frameworks, outlines the major industrial clusters and projects under development, and evaluates the strategic importance of CCUS within the UK’s broader decarbonisation agenda.

Policy Framework and Government Support

The UK government has implemented a comprehensive policy framework to accelerate the development of CCUS infrastructure and projects. Central to this strategy is the cluster sequencing process, which identifies regions where industrial emissions can be captured and transported to shared storage facilities. This approach reflects the geographical concentration of industrial activity within the UK; approximately seven major industrial clusters produce around half of all industrial emissions in the country.

The cluster sequencing programme is divided into multiple phases. The first phase, known as Track-1, selected two clusters for early deployment: the HyNet cluster in north-west England and North Wales, and the East Coast Cluster centred on Teesside and the Humber region. Subsequent phases aim to bring additional clusters online by the end of the decade, including the Acorn cluster in Scotland and the Viking cluster in the Humber region.

Government investment has been substantial. In 2024 the UK committed approximately £21.7 billion over 25 years to support the development of CCUS projects and associated infrastructure. This funding is designed to reduce financial risks for early-stage projects and create a commercially viable market for carbon capture services.

An additional mechanism supporting this effort is the Carbon Capture and Storage Infrastructure Fund (CIF), which provides around £1 billion in capital funding for transport and storage infrastructure. The CIF focuses particularly on the early stages of CCUS deployment by financing pipelines, offshore storage sites and initial industrial capture projects.

The government’s longer-term objective is to establish a competitive carbon capture market by the mid-2030s. This includes regulatory frameworks, revenue support mechanisms, and business models designed to attract private investment. The sector is expected to contribute significantly to the economy, potentially adding billions of pounds in economic value and supporting tens of thousands of jobs.

Beyond climate policy, CCUS also plays an important role in the UK’s industrial strategy. Many traditional manufacturing regions face economic challenges due to decarbonisation pressures. Carbon capture offers a pathway to maintain industrial activity while reducing emissions, helping to sustain employment and investment in areas historically dependent on heavy industry.

Major Carbon Capture Clusters

The UK’s CCUS deployment strategy is centred on industrial clusters where multiple emitters can connect to shared transport and storage infrastructure. This approach significantly reduces costs compared with standalone projects and allows emissions from multiple facilities to be aggregated and managed collectively.

The first cluster selected for deployment is HyNet North West. This project spans north-west England and North Wales and focuses on capturing emissions from industrial sites such as refineries, chemical plants, cement facilities and waste-to-energy plants. Captured CO₂ will be transported through pipeline networks to depleted gas fields in Liverpool Bay, where it will be permanently stored beneath the seabed.

HyNet is considered one of the most advanced carbon capture projects in Europe. The transport and storage infrastructure for the project reached financial close in 2025, allowing construction to proceed. The development is expected to generate significant supply chain activity and support thousands of jobs across the region.

The second major cluster is the East Coast Cluster, which covers Teesside and the Humber region. This cluster includes several major decarbonisation initiatives, including the Net Zero Teesside project. Net Zero Teesside aims to develop a gas-fired power station equipped with carbon capture technology, alongside CO₂ transport infrastructure and offshore storage facilities beneath the North Sea.

Once operational, the East Coast Cluster is expected to capture millions of tonnes of CO₂ annually from power generation and heavy industry. The cluster also forms a key component of the UK’s strategy for developing low-carbon hydrogen production, as hydrogen derived from natural gas can be produced with minimal emissions when combined with carbon capture.

The development of these clusters marks the transition of CCUS in the UK from conceptual planning to large-scale deployment. With financial close achieved for the first projects and construction beginning in the mid-2020s, the UK is moving toward establishing a fully operational carbon capture industry.

Emerging Projects and Future Clusters

Beyond the initial Track-1 clusters, the UK government is supporting several additional CCUS projects that could form the next wave of carbon capture deployment.

One of the most significant is the Acorn project in north-east Scotland, centred on the St Fergus gas terminal. The project plans to capture emissions from industrial sources and transport the CO₂ through existing offshore pipelines for storage beneath the North Sea. The project could store around five million tonnes of CO₂ annually by 2030.

The Acorn development benefits from extensive offshore infrastructure created during decades of oil and gas production. Repurposing these pipelines and reservoirs reduces development costs and accelerates project timelines. The UK government has already committed hundreds of millions of pounds in support of the project as part of its broader CCUS investment programme.

Another major proposed cluster is the Viking CCS project in the Humber region. This project would utilise depleted gas fields beneath the North Sea to store carbon captured from nearby industrial facilities. Combined with other clusters, Viking could significantly expand the UK’s national CO₂ storage capacity.

Additional carbon capture initiatives are also emerging in sectors such as cement production and waste-to-energy facilities. These projects target industries where emissions are difficult to eliminate through conventional decarbonisation technologies. By capturing emissions at source, CCUS enables these industries to continue operating while meeting climate targets.

The UK’s long-term ambition is to capture and store between 20 and 30 million tonnes of CO₂ annually by 2030. Achieving this goal will require rapid expansion of capture capacity and the development of extensive CO₂ transport networks linking industrial emitters with offshore storage sites.

Challenges and Criticisms

Despite strong government support, the development of carbon capture in the UK faces several economic and technological challenges. CCUS projects are capital-intensive and require complex infrastructure, including capture facilities, pipeline networks and offshore injection sites. These high upfront costs have historically hindered project development.

The commercial viability of carbon capture also depends heavily on government subsidies and regulatory frameworks. Without revenue support mechanisms such as carbon pricing or contractual payments for captured CO₂, many projects would struggle to attract private investment.

There are also technological risks associated with large-scale carbon storage. Monitoring and verification systems must ensure that injected CO₂ remains securely contained underground. Researchers have highlighted the need for improved monitoring technologies, including offshore seismic monitoring networks, to detect potential leaks or geological disturbances.

Some critics argue that carbon capture may prolong the use of fossil fuels rather than accelerating the transition to renewable energy. The technology is often associated with natural gas power generation and hydrogen production from fossil fuels, which raises concerns about long-term reliance on hydrocarbons.

Project uncertainty also remains an issue. Some planned initiatives have been delayed or cancelled due to changing market conditions or shifts in government priorities. For example, certain hydrogen and carbon capture proposals in the Teesside region have faced setbacks due to economic and industrial factors.

Nevertheless, proponents argue that carbon capture is essential for achieving net-zero emissions, particularly for industrial sectors that cannot easily transition to electrification or renewable energy sources.

Conclusion

Carbon capture has become a central pillar of the United Kingdom’s strategy to decarbonise its economy while maintaining industrial competitiveness. The government’s cluster-based approach, combined with substantial financial support and regulatory frameworks, has created one of the most advanced CCUS development programmes in Europe.

Major clusters such as HyNet and the East Coast Cluster are now progressing from planning to construction, marking a significant milestone for the industry. Additional projects, including the Acorn and Viking clusters, could further expand the UK’s carbon capture capacity in the coming decade.

If successfully implemented, these projects could enable the UK to capture tens of millions of tonnes of carbon dioxide annually by 2030. This would play a critical role in reducing emissions from heavy industry, supporting low-carbon hydrogen production, and achieving national climate targets.

However, the sector still faces substantial challenges. High capital costs, technological uncertainties and policy dependence mean that continued government support will remain essential during the early stages of deployment. Ensuring public confidence in the safety and effectiveness of carbon storage will also be crucial.

Overall, the development of carbon capture infrastructure represents both an environmental necessity and an economic opportunity for the United Kingdom. By leveraging its industrial base, offshore geology and energy expertise, the UK has the potential to become a global leader in carbon capture technology and services.

Major Carbon Capture Projects in the United Kingdom

Introduction

Carbon capture, utilisation and storage (CCUS) has become a central element of the United Kingdom’s strategy to reduce industrial greenhouse gas emissions and meet its legally binding target of achieving net-zero emissions by 2050. The technology captures carbon dioxide (CO₂) from industrial processes or power generation before it enters the atmosphere. The captured CO₂ is then transported—typically through pipelines or shipping infrastructure—to geological formations where it can be stored permanently underground, often in depleted oil and gas reservoirs or deep saline aquifers.

The United Kingdom is particularly well positioned to deploy CCUS due to several structural advantages. The country possesses extensive offshore geological storage capacity in the North Sea, a large concentration of industrial clusters that emit significant volumes of CO₂, and decades of expertise in offshore engineering developed through the oil and gas industry. These factors have enabled the UK government and industry stakeholders to pursue a cluster-based model for carbon capture deployment.

The UK’s CCUS strategy focuses on linking industrial emitters to shared transport and storage infrastructure. Rather than building isolated capture facilities, the cluster model aggregates emissions from multiple facilities within major industrial regions, reducing infrastructure costs and improving project viability. The government’s ambition is to capture between 20 and 30 million tonnes of CO₂ annually by 2030 through a network of clusters and storage projects.

This report examines key carbon capture projects currently under development in the United Kingdom, drawing on reporting and project updates published by KeyFacts Energy and related industry sources. It highlights the major clusters, industrial capture facilities and emerging storage projects that together form the backbone of the UK’s CCUS strategy.

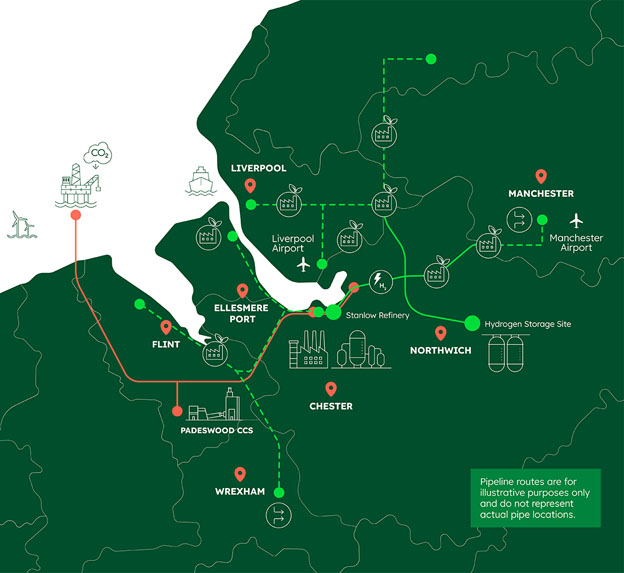

The HyNet North West Cluster

The HyNet North West project is one of the most advanced carbon capture clusters in the United Kingdom and represents a cornerstone of the country’s early CCUS deployment. The cluster spans northwest England and North Wales, an area characterised by high levels of industrial activity including oil refining, chemicals manufacturing, cement production and energy generation.

At the core of the HyNet cluster is the Liverpool Bay carbon storage system, which will transport captured carbon dioxide from industrial facilities to depleted gas fields beneath the seabed for permanent storage. The infrastructure involves both new and repurposed pipelines as well as compression facilities that will prepare the CO₂ for offshore injection.

The Liverpool Bay storage development has attracted major investment from energy companies and contractors. Engineering company Saipem, for example, has been awarded a contract to convert the existing gas compression and treatment facility at Point of Ayr in North Wales into a dedicated CO₂ compression station. This facility will compress captured carbon dioxide before it is transported to offshore storage reservoirs.

The HyNet cluster will serve a wide range of industrial emitters across the region. One notable project is the carbon capture facility being developed at the Heidelberg Materials cement plant in Padeswood, North Wales. The plant is expected to capture approximately 800,000 tonnes of CO₂ annually, representing nearly all of the facility’s emissions. The captured CO₂ will then be transported via pipeline to storage sites in Liverpool Bay as part of the wider HyNet infrastructure network.

In addition to the cement facility, HyNet will support carbon capture installations at refineries, hydrogen production plants and waste-to-energy facilities. Collectively, these projects are expected to significantly reduce emissions from one of the UK’s most carbon-intensive industrial regions while supporting economic activity and job creation across northwest England and North Wales.

The East Coast Cluster and the Northern Endurance Partnership

The Northern Endurance Partnership (NEP) is developing onshore and offshore infrastructure needed to transport CO2 from carbon capture projects across Teesside and the Humber – collectively known as the East Coast Cluster - to secure storage under the North Sea.

The infrastructure is crucial to achieving net zero in the UK’s most carbon intensive industrial regions.

NEP, via the Endurance saline aquifer and adjacent stores, has access to up to 1 billion tonnes of CO₂ storage capacity.

NEP is in an incorporated joint venture established solely to develop and operate CO₂ transportation and storage infrastructure on behalf of the NEP Shareholders – bp, Equinor and TotalEnergies.

The East Coast Cluster is the second flagship carbon capture project selected by the UK government in the initial phase of its CCUS cluster sequencing programme. Located along the northeast coast of England, the cluster encompasses two major industrial regions: Teesside and the Humber.

The cluster will rely on a large offshore storage system centred on the Endurance saline aquifer beneath the North Sea. The storage site is being developed by the Northern Endurance Partnership (NEP), a consortium responsible for the transportation and storage infrastructure for captured carbon emissions in the region.

The Endurance storage site lies approximately 75 kilometres offshore and has the capacity to store up to 100 million tonnes of CO₂ over a 25-year period. Captured emissions from industrial facilities across Teesside and the Humber will be transported to the site through a network of pipelines before being injected deep beneath the seabed.

A central project within the East Coast Cluster is the Net Zero Teesside Power development. This project aims to build a gas-fired power station equipped with carbon capture technology capable of generating up to 860 megawatts of low-carbon electricity. The facility will capture and store around two million tonnes of CO₂ annually while providing flexible power generation that supports intermittent renewable energy sources such as wind and solar.

Several other industrial capture projects are expected to connect to the East Coast Cluster over time, including steel production, chemical manufacturing and hydrogen production facilities. By linking these emitters to shared storage infrastructure, the cluster aims to decarbonise one of the UK’s largest industrial regions while maintaining energy security and industrial competitiveness.

In March 2026, NSTA granted consent to drill a carbon storage appraisal well which could become a build-out of the Endurance project off the coast of Teesside.

It is another important step forward in helping the growing industry reach first injection and meet government targets of storing 100 million tonnes of CO2 per year, which the Climate Change Committee calculates is vital for the UK to meet net zero by 2050.

Track-2 Carbon Capture Projects: Acorn and Viking

While the HyNet and East Coast clusters represent the first wave of CCUS deployment, the UK government is also supporting additional projects that could form the next stage of the national carbon capture network.

One of the most prominent of these developments is the Acorn carbon capture and storage project in northeast Scotland. Located at the St Fergus gas terminal, the project aims to capture emissions from industrial facilities and store the CO₂ beneath the North Sea using existing offshore pipelines and reservoirs originally developed for oil and gas production.

The Acorn project is designed to store approximately five million tonnes of CO₂ per year by 2030. Its strategic location and existing infrastructure make it one of the most cost-effective potential CCS developments in the UK.

The UK government has committed significant financial support to the project, including an investment of approximately £200 million to accelerate development and support the construction of transport and storage infrastructure.

Another major Track-2 project is the Viking CCS development in the Humber region. The project will utilise depleted gas fields beneath the North Sea to store carbon emissions captured from industrial sites in northern England. Viking is expected to play a key role in expanding the UK’s CO₂ storage capacity and supporting decarbonisation across heavy industry.

Together, the Acorn and Viking projects could capture and store up to 18 million tonnes of CO₂ annually once fully operational, significantly increasing the UK’s national carbon storage capacity.

Emerging Carbon Capture Initiatives

Alongside the large cluster developments, several smaller carbon capture projects and pilot initiatives are emerging across the UK. These projects are often focused on specific industrial sectors or testing new capture technologies that could be deployed more widely in the future.

Energy-from-waste operator enfinium has launched pilot carbon capture projects at several of its facilities as part of a broader programme to deploy CCS across its operations. The company plans to invest around £1.7 billion in carbon capture technology and has initiated pilot projects at facilities including Parc Adfer in North Wales and Ferrybridge in West Yorkshire.

These pilot projects are designed to test next-generation capture technologies and evaluate their performance in operational waste-to-energy facilities. The initiatives aim to generate data on capture efficiency, solvent performance and operational reliability, providing valuable insights for future commercial deployments.

Another emerging development is the Poseidon carbon storage project in the Southern North Sea. The project plans to utilise the Leman gas field as a storage site capable of injecting approximately 1.5 million tonnes of CO₂ annually during its initial phase, with the potential to expand significantly over time.

Additional storage developments are also being explored in regions such as Shetland, where infrastructure at the Sullom Voe terminal could support large-scale CO₂ storage projects linked to both UK and European emissions sources. These projects highlight the growing role of the North Sea as a major hub for carbon storage.

Economic and Strategic Importance

Carbon capture projects are expected to play a major role in the UK’s energy transition and industrial strategy. The government estimates that the development of CCUS infrastructure could contribute around £5 billion annually to the UK economy by 2050 while supporting up to 50,000 long-term jobs across the energy and industrial sectors.

The sector is also expected to generate substantial supply chain activity in engineering, construction, offshore services and environmental monitoring. Many of the companies involved in CCUS projects—such as engineering contractors, technology providers and offshore service firms—draw on expertise originally developed within the oil and gas industry.

The development of carbon capture infrastructure may also position the UK as a regional hub for CO₂ storage. With extensive offshore storage capacity and established pipeline networks, the UK could potentially store carbon emissions captured in other European countries in addition to domestic emissions.

However, significant challenges remain. Carbon capture projects require large capital investments and complex regulatory frameworks, and many projects depend on government subsidies and long-term policy stability. The success of the UK’s CCUS programme will therefore depend on sustained collaboration between government, industry and investors.

Viking CCS Project (Humber)

The Viking CCS Project is a large-scale carbon capture and storage (CCS) initiative planned for the United Kingdom’s Humber region and the southern North Sea. Its purpose is to capture carbon dioxide emissions from heavy industries and power generation, transport the CO₂ through pipelines, and permanently store it deep underground in depleted gas fields beneath the seabed. The project is part of the UK government’s broader strategy to decarbonise industrial regions while maintaining energy-intensive industries such as chemicals, refining, cement, and power generation.

The project is centred on the Humber industrial cluster, which is one of the largest concentrations of industrial emissions in the UK. Carbon dioxide captured from factories and power plants will be transported through a new pipeline network to the Lincolnshire coast. From there, offshore pipelines will carry the CO₂ into geological storage sites beneath the southern North Sea. These storage sites are mainly depleted natural gas reservoirs that have previously held hydrocarbons securely for millions of years, making them suitable for long-term CO₂ storage.

A key element of the project is the repurposing of existing gas infrastructure. The offshore storage system will make use of the former Viking gas fields, which historically produced natural gas but are now largely depleted. By converting these reservoirs into storage sites, the project can significantly reduce development costs and accelerate deployment compared with building entirely new infrastructure.

The development is being led by Harbour Energy, the largest independent oil and gas producer in the UK, together with partners including BP and Phillips 66. Their goal is to build a shared CO₂ transport and storage network that multiple industrial emitters can connect to over time. This “open-access” model is intended to allow different companies in the region to decarbonise their operations without each building their own capture and storage infrastructure.

In terms of scale, the project is expected to store tens of millions of tonnes of CO₂ over its lifetime. Early phases aim to capture and store around 10 million tonnes of carbon dioxide per year by the early 2030s, with potential expansion to significantly higher volumes as more emitters connect to the network. This scale would make it one of the largest carbon storage hubs in Europe.

The project is also closely tied to UK climate policy. The UK government views carbon capture and storage as essential for achieving its legally binding net-zero emissions target by 2050, particularly in sectors where electrification is difficult. The Viking CCS project was therefore selected as one of the priority clusters in the UK’s carbon capture deployment programme, alongside other major initiatives such as HyNet North West and East Coast Cluster.

Beyond emissions reduction, the project is expected to support regional economic activity by preserving industrial jobs in the Humber region and creating new roles in pipeline construction, offshore operations, and carbon management. By reusing existing energy infrastructure and geological resources, it also represents an attempt to transition parts of the UK’s oil and gas sector toward supporting a low-carbon economy.

Overall, the Viking CCS project illustrates how carbon capture infrastructure can be integrated into existing industrial and offshore energy systems to reduce emissions while maintaining large-scale industrial production.

Drax BECCS (Bioenergy with Carbon Capture and Storage)

The Drax BECCS is a proposed large-scale carbon removal project in the United Kingdom that combines biomass power generation with carbon capture and storage (BECCS). The project is being developed at the Drax Power Station, the UK’s largest renewable power station, located near Selby in North Yorkshire. Its goal is to generate electricity from sustainably sourced biomass while capturing and permanently storing the carbon dioxide released during combustion, thereby removing carbon from the atmosphere.

Bioenergy with carbon capture works by taking advantage of the natural carbon cycle. Trees and other plants absorb carbon dioxide from the atmosphere as they grow. When biomass such as compressed wood pellets is burned to generate electricity, the captured carbon is released again as CO₂. In a BECCS system, however, that CO₂ is captured before it enters the atmosphere, compressed, and transported to a geological storage site where it is permanently stored underground. Because the carbon originally came from the atmosphere through plant growth, capturing and storing it results in net negative emissions.

At Drax, the plan is to install carbon capture technology on two of the biomass-generating units at the power station. The captured CO₂ would then be transported through a pipeline network to offshore storage locations beneath the North Sea. One of the proposed storage routes involves the Viking CCS Project, which aims to store CO₂ in depleted gas reservoirs under the seabed. Integrating BECCS with regional CO₂ transport and storage infrastructure allows the captured carbon to be handled at industrial scale.

The project is being developed by Drax Group, which converted most of the former coal-fired power station to biomass over the past decade. Drax argues that adding carbon capture to its biomass units could remove millions of tonnes of CO₂ from the atmosphere each year while continuing to supply dispatchable electricity to the grid. The company has stated that the BECCS system could capture around eight million tonnes of CO₂ annually once fully operational, potentially making it one of the largest carbon removal facilities in the world.

The project is also closely connected to the UK’s climate strategy. The UK government considers engineered carbon removals necessary to reach its legally binding net-zero target by 2050, particularly to offset emissions from sectors such as aviation and agriculture that are difficult to fully decarbonise. BECCS is one of the main technologies being considered for this role because it can simultaneously generate electricity and remove carbon from the atmosphere.

Despite its potential climate benefits, the project has generated debate. Supporters argue that it could play a crucial role in achieving negative emissions at scale while supporting energy security and jobs in northern England. Critics question the sustainability of large-scale biomass supply chains, the lifecycle emissions associated with harvesting and transporting wood pellets, and the long-term effectiveness of relying on carbon capture. These discussions reflect wider international debates about the role of BECCS in global climate mitigation strategies.

Overall, the Drax BECCS project represents an attempt to transform an existing large biomass power station into a facility capable of delivering both renewable electricity and large-scale carbon removal. If implemented as planned, it would form part of the emerging UK carbon capture and storage network and could become a key component of the country’s pathway to net-zero emissions.

Conclusion

Carbon capture and storage is emerging as a critical technology within the United Kingdom’s strategy to achieve net-zero emissions while maintaining industrial competitiveness. The development of major clusters such as HyNet and the East Coast Cluster represents the first stage of a nationwide CCUS network that will capture emissions from heavy industry and power generation.

These flagship projects are complemented by a second wave of developments, including the Acorn and Viking clusters, as well as smaller industrial capture projects and pilot initiatives across multiple sectors. Together, these projects demonstrate the growing momentum behind carbon capture deployment in the UK.

If successfully implemented, the UK’s CCUS programme could establish the country as a global leader in carbon storage and industrial decarbonisation. The combination of favourable geology, offshore engineering expertise and strong government support provides a foundation for large-scale deployment over the coming decades.

Ultimately, the success of carbon capture in the UK will depend on continued investment, technological innovation and the effective integration of capture, transport and storage infrastructure. As projects move from planning to construction and operation, the coming decade will be critical in determining the role that carbon capture will play in the UK’s long-term energy transition.

KeyFacts Energy news: Carbon Capture and Storage