By Dipo Oladehinde, Head of Energy desk at BusinessDay

Nigeria’s oil sector is a shadow of its bustling self as foreign direct investment (FDI) plummets from billions of dollars to mere trickles in millions.

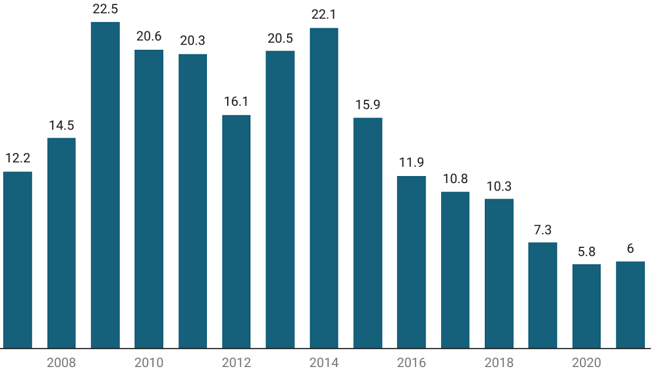

FDI in the sector fell to less than half a billion dollars in the first half of 2023, with the full-year figure unlikely to match a peak of $22.5 billion in 2019.

When an oil executive said Nigeria needed $25 billion per annum in investments to be able to achieve a production target of 2 million barrels daily, the task at hand for Nigeria came into better perspective.

The 2010s witnessed a period of significant FDI from international companies eager to tap into the country’s vast oil and gas reserves as the future for Nigeria’s nascent indigenous upstream oil and gas industry looked bright, almost dazzlingly so.

FDI in Nigeria's oil and gas sector ($bn)

Chart: BusinessDay - created with Datawrapper

In 2014, Nigeria attracted the largest amount of FDI of any African country, with inflows exceeding $22.1 billion. This influx of capital fueled major projects, including deepwater exploration and development of new oil fields.

Oil was selling for more than $100 a barrel, as much as twice the production costs in Nigeria’s trickiest deepwater fields and several multiples of those in its shallow water and onshore fields.

Nigeria’s oil rigs, which depicts the level of oil fields averaged 35 rig counts in 2014, a development that translated to increased crude production as Nigeria’s output averaged 2.2 million barrels per day.

In August 2014 “the perfect storm of collapsing oil prices” arrived, said Carlos Hardenberg, lead portfolio manager of Templeton Emerging Markets Investment Trust. The naira fell, investors fled and Niger Delta militants who wanted a greater share of the country’s energy wealth struck.

Little has changed since then.

The country’s appeal had been tarnished by security problems that have only worsened since.

Compounding this internal rot is the exodus of oil majors such as Shell, ExxonMobil, Eni and TotalEnergies that once buzzed with the rhythm of the pumps, now echo with the silence of departure.

The pain of this large-scale theft and vandalism, as well as decades of under-investment in infrastructure, was so severe that in April 2023, the country produced less than one million barrels of oil daily, far below its 1.8m bpd Organisation of Petroleum Exporting Countries quota.

In March, Nigeria’s oil production stood at 1.23m bpd.

“Nigeria currently needs $25 billion annually to stabilise its oil production at 2 million bpd,” Austin Avuru, executive chairman of AA Holdings said at the Harvard Business School (Association of Nigeria) event in Nigeria’s commercial capital.

The Nigerian oil and gas industry was totally sidelined by foreign investors in the second quarter of 2023 for the first time on record with zero FDI, as the once lucrative sector attracted no capital inflow in the latest review quarter.

In the first quarter of 2023, oil FDI stood at a mere $750,000.

Article source: BusinessDay